|

|

Clients, friends, and colleagues:

Before we dive into the new numbers in San Francisco, I thought I'd relay some quick insights from my day-to-day talks with clients, writing offers, holding open houses, touring, etc.

While this market remains dynamic, there's a sense of normalcy in many sectors. I realize that "normal" is an odd term to use during a time where dramatic headlines will tell you quite the contrary, but in terms of activity, many districts of our market feel relatively balanced. Interest rates in the 6% range are no longer a debilitating shock to demand, inventory levels actually aren't too far off of pre-pandemic norms, and property is still selling. It's when you compare today's data to 2021 and 2022 (especially Q1 2022) that the comparisons are dramatic. Note that SoMa/South Beach are uniquely slow -- I've seen several recent sales that approach prices that date as far back as 2014 levels. I attribute this to higher levels of supply and the continued effects of remote work.

I've witnessed some very surprising overbids, and I've also written offers for clients that I was genuinely surprised to see get accepted. My buyers who named their price and stayed conservative secured some wonderful values.

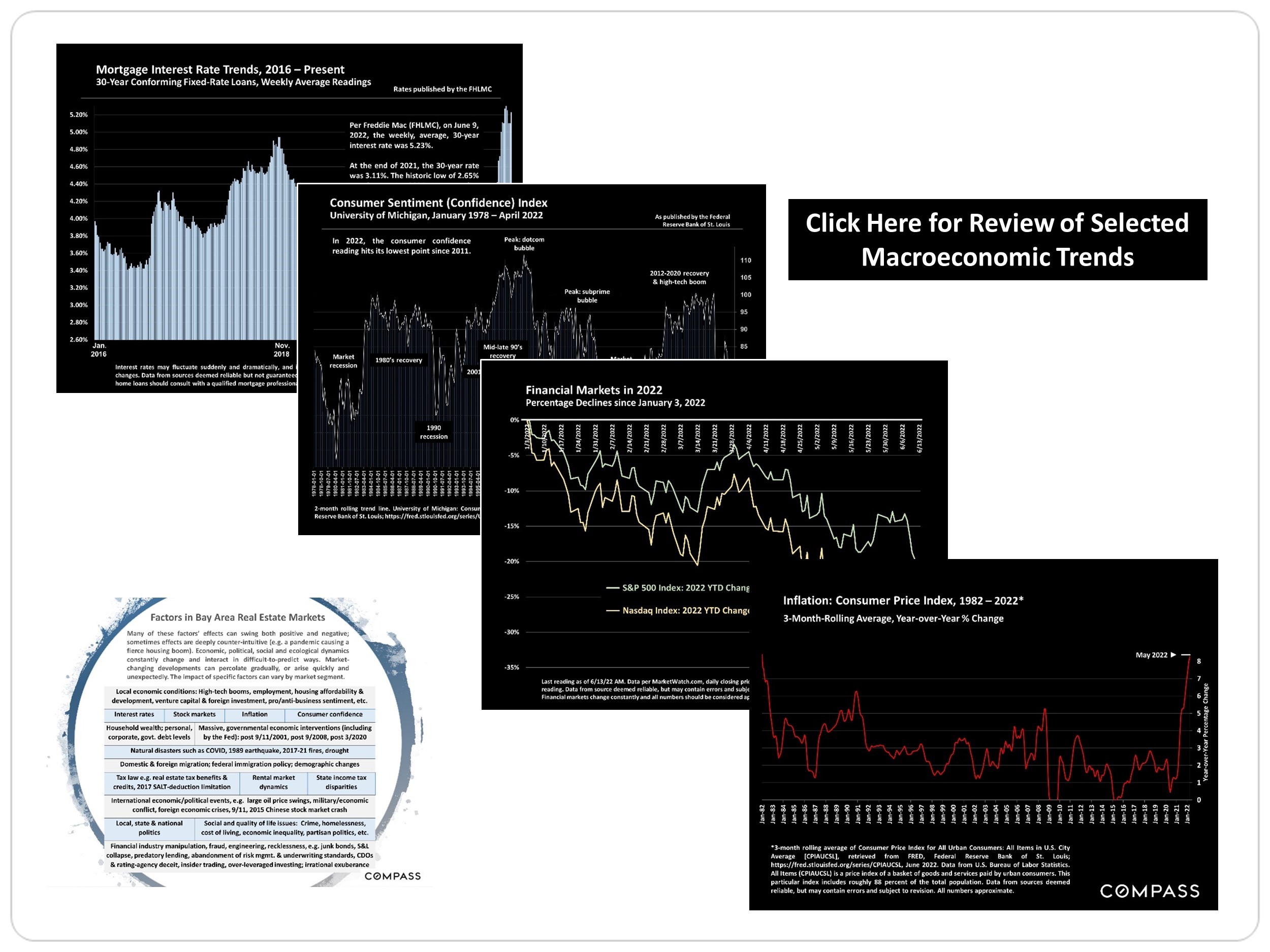

Without a doubt, interest rates remain the key factor in every sector of our market, and is the most important metric to watch.

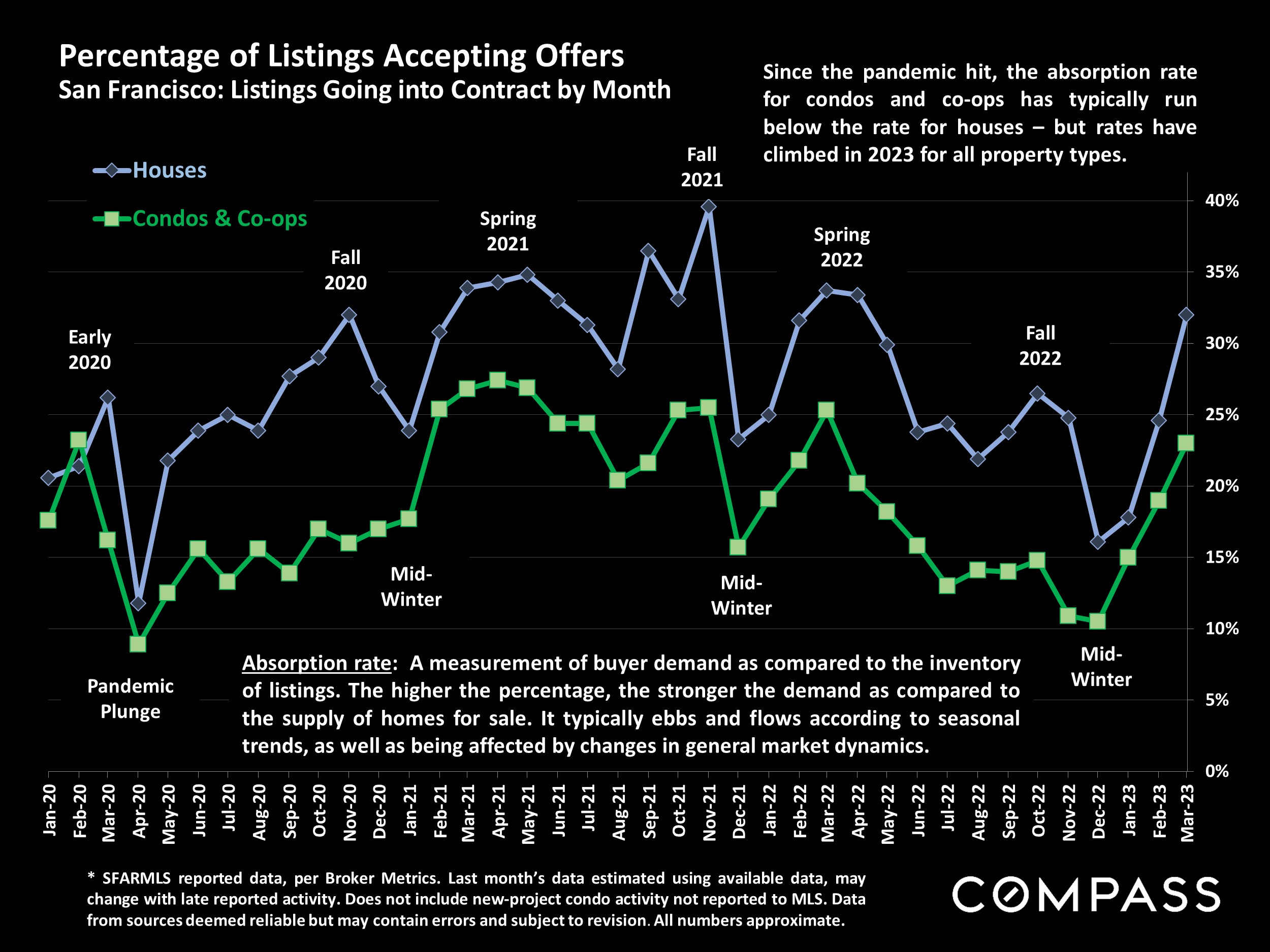

Buyer demand continued to rebound from the depths of the mid-winter slowdown: The number and percentage of listings going into contract and overbidding percentages continued to climb, while days-on-market dropped as the spring selling season gained traction. Buyers generally shrugged off the local banking crisis, the main effect of which, so far, has been a significant drop in interest rates in the 4 weeks after SVB collapse and First Republic first came under pressure.

Though conditions have improved considerably, the market remains significantly weaker on a year-over-year basis, and across the Bay Area, median sale prices have declined. However it's worth remembering that the market in Q1 2022 was wildly overheated and approaching the peak of a historic 10-year boom. Since this will distort many year-over-year comparisons, I've provided key metrics below that track the past 5 years:

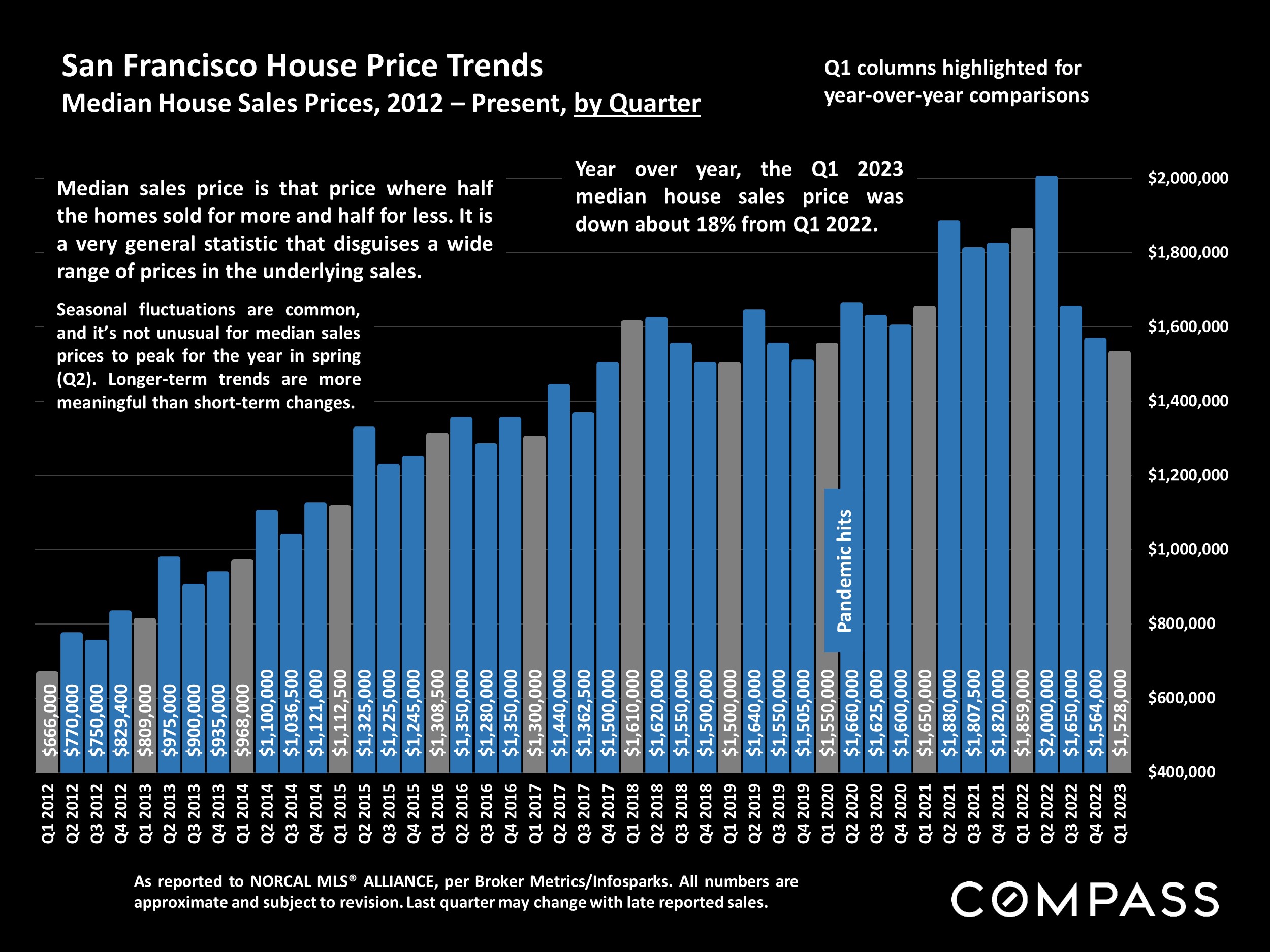

San Francisco Single-Family Home Sales (using 3-month rolling data):

March 2023: $1,528,000 (down 17.8%)

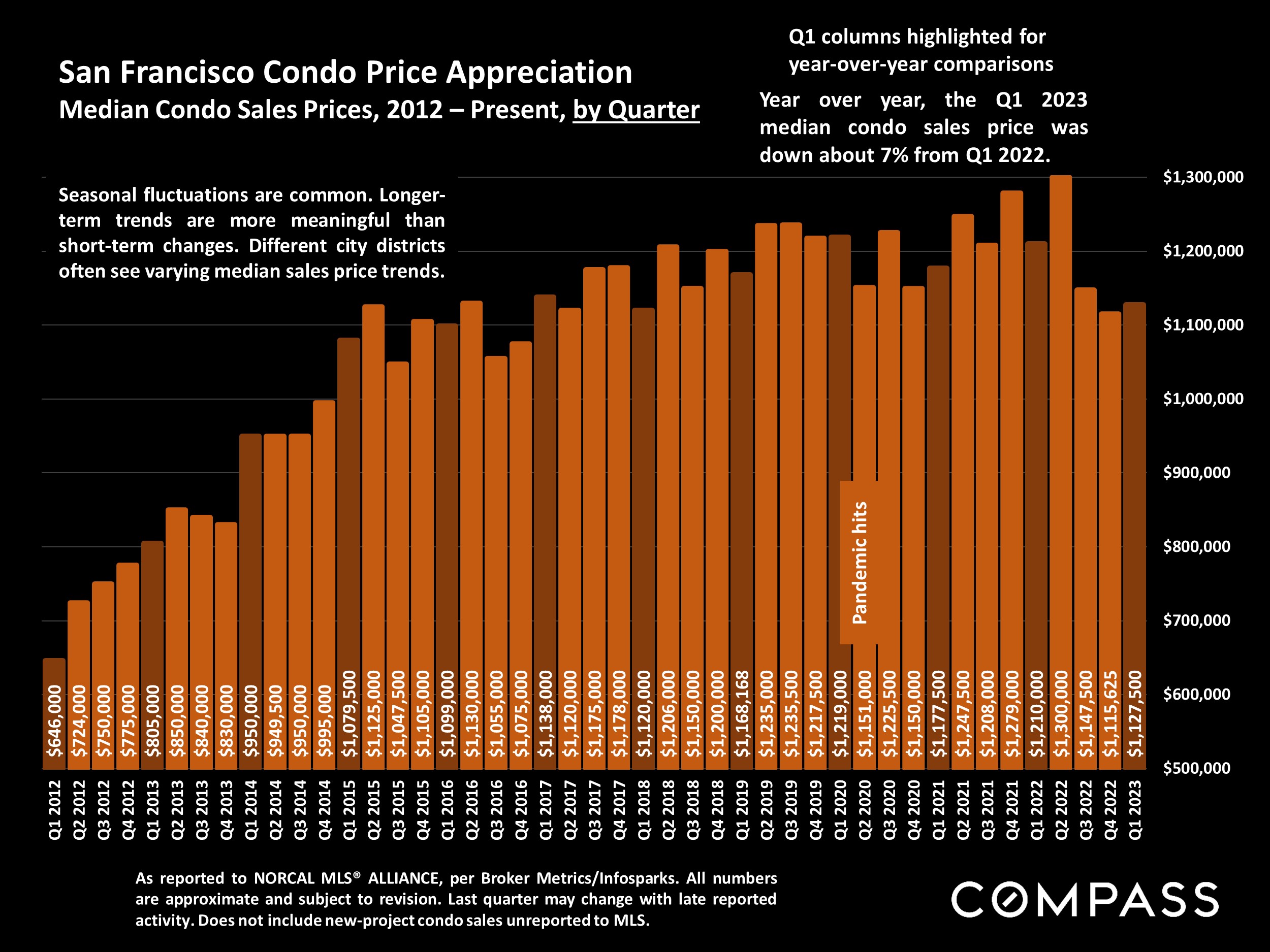

San Francisco Condo Sales (using 3-month rolling data):

March 2023: $1,120,000 (down 7.4%)

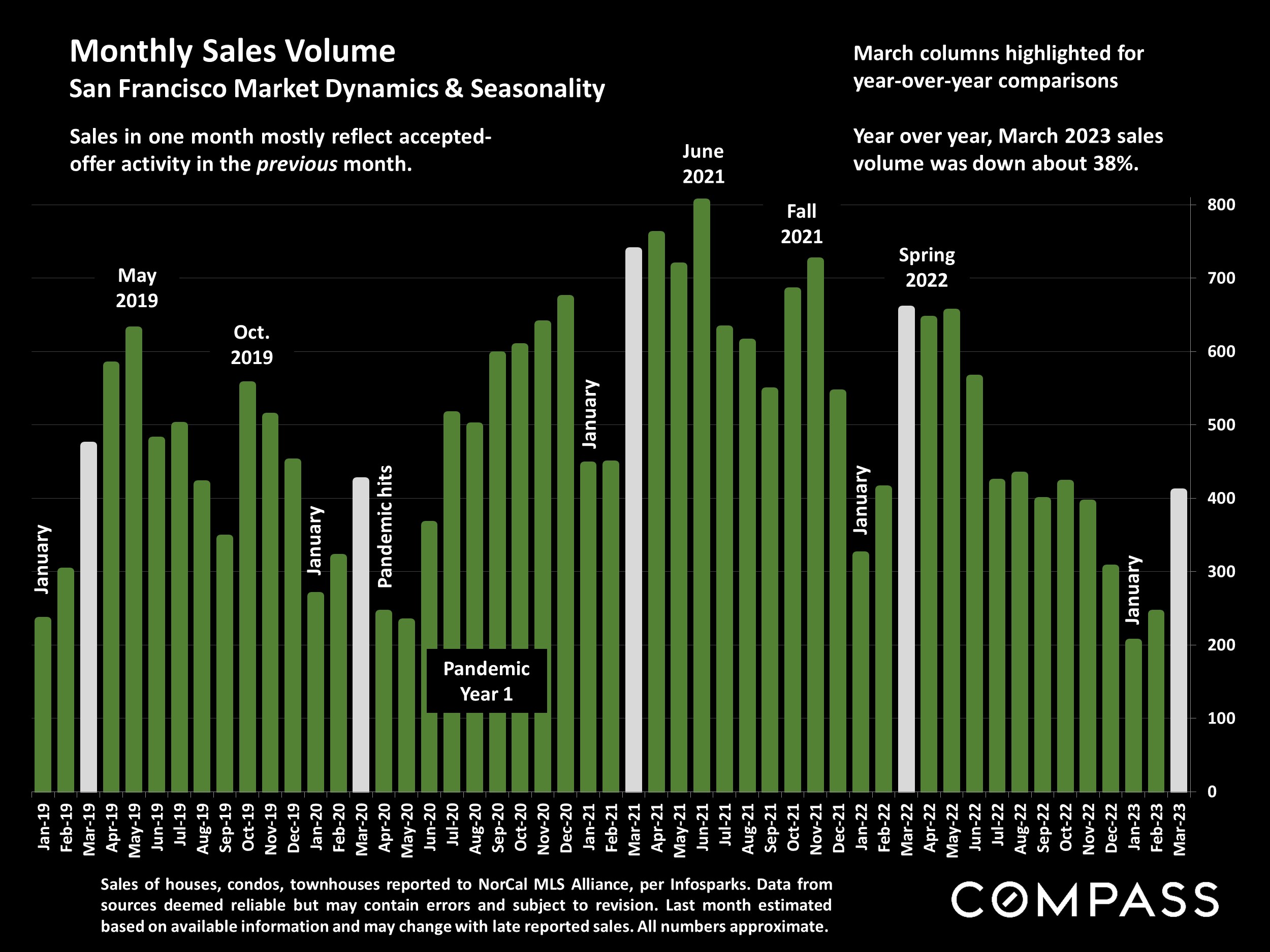

March 2023: 420 (down 43%)

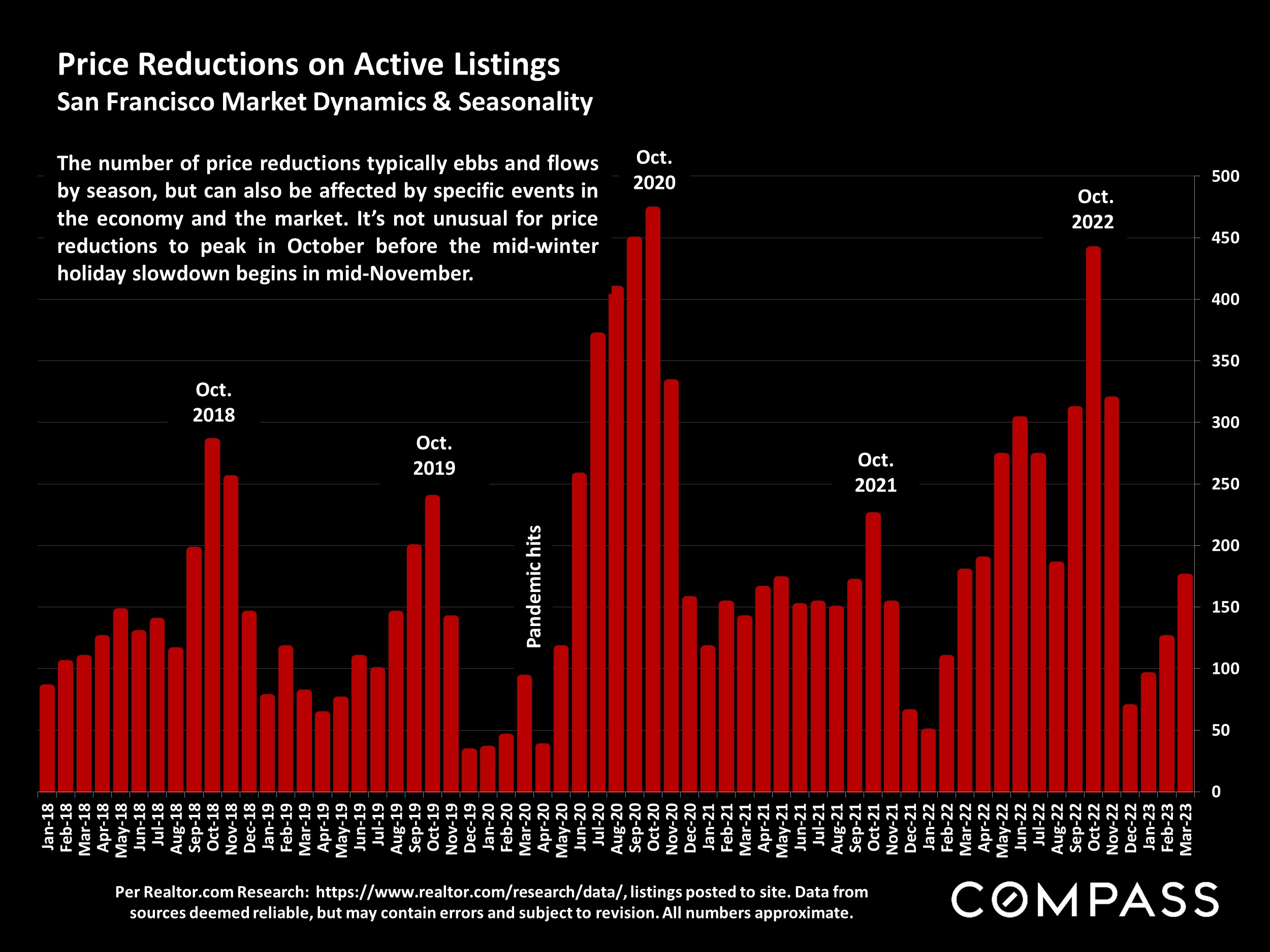

The number of new listings coming on market continues to be extremely low, as many potential sellers hold off from listing their homes due to the doubling of interest rates since early 2022: This constitutes a huge factor in market dynamics and is undoubtedly holding back sales activity.

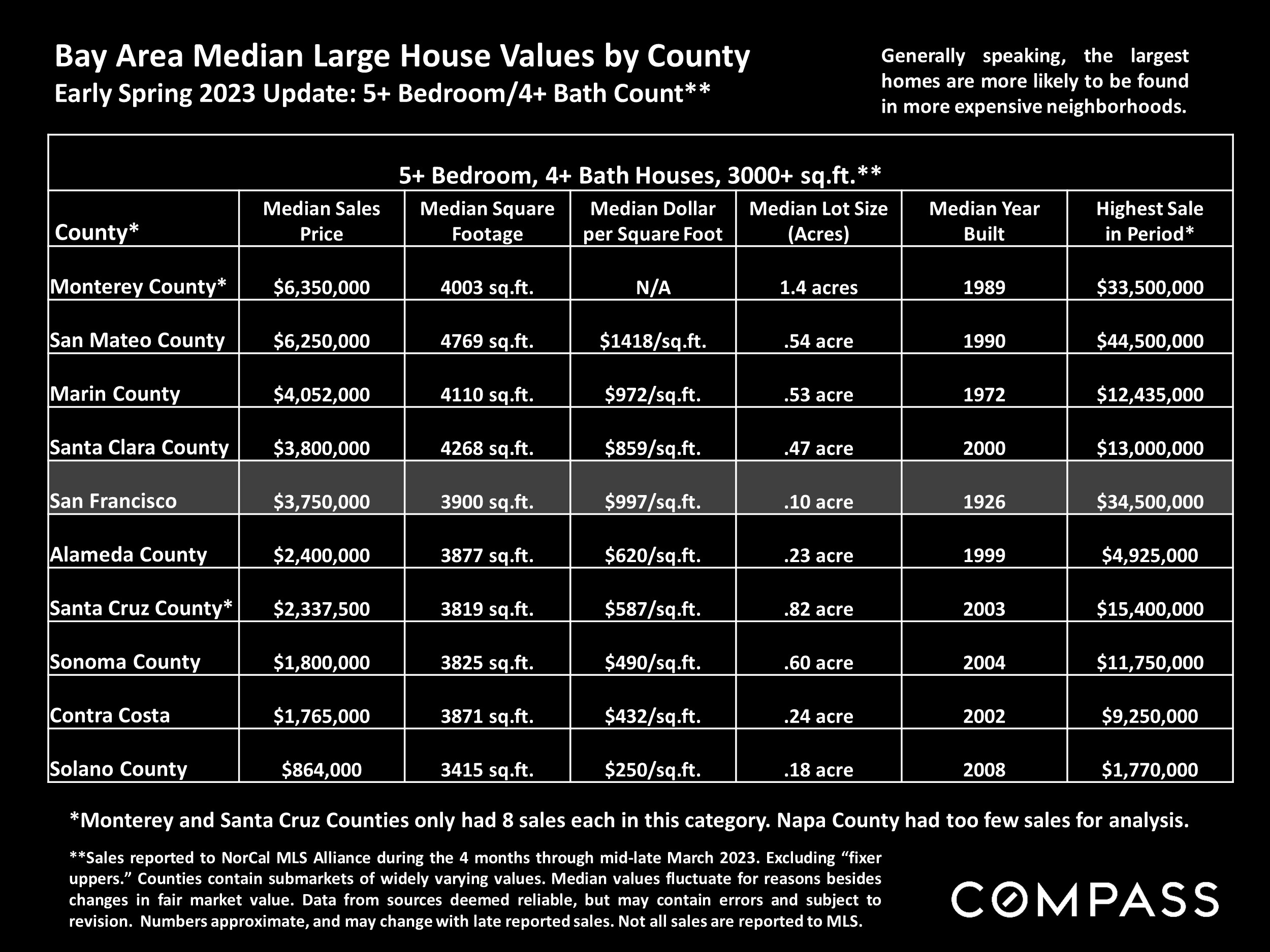

Across the Bay Area, year-over-year sales declines in the highest price segments have outpaced drops for less expensive homes, and their demand-to-supply ratio - the number of sales compared to the number of listings for sale - is much weaker. Luxury home sales have been hit harder since the market correction began in mid-2022, though they too have been rebounding in 2023.

April, May, & June sales volumes are commonly among the highest of the year, and this is especially true for luxury home sales.

I am always here if you have any questions about the market, or a specific property.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statistics are generalities, essentially summaries of widely disparate data generated by dozens, hundreds or thousands of unique, individual sales occurring within different time periods. They are best seen not as precise measurements, but as broad, comparative indicators, with reasonable margins of error. Anomalous fluctuations in statistics are not uncommon, especially in smaller, expensive market segments. Last period data should be considered estimates that may change with late-reported data. Different analytics programs sometimes define statistics - such as "active listings," "days on market," and "months supply of inventory" - differently: what is most meaningful are not specific calculations but the trends they illustrate. Most listing and sales data derives from the local or regional multi-listing service (MLS) of the area specified in the analysis, but not all listings or sales are reported to MLS and these won't be reflected in the data. "Homes" signifies real-property, single-household housing units: houses, condos, co-ops, townhouses, duets and TICs (but not mobile homes), as applicable to each market. City/town names refer specifically to the named cities and towns, or their MLS areas, unless otherwise delineated. Multicounty metro areas will be specified as such. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers to be considered approximate.

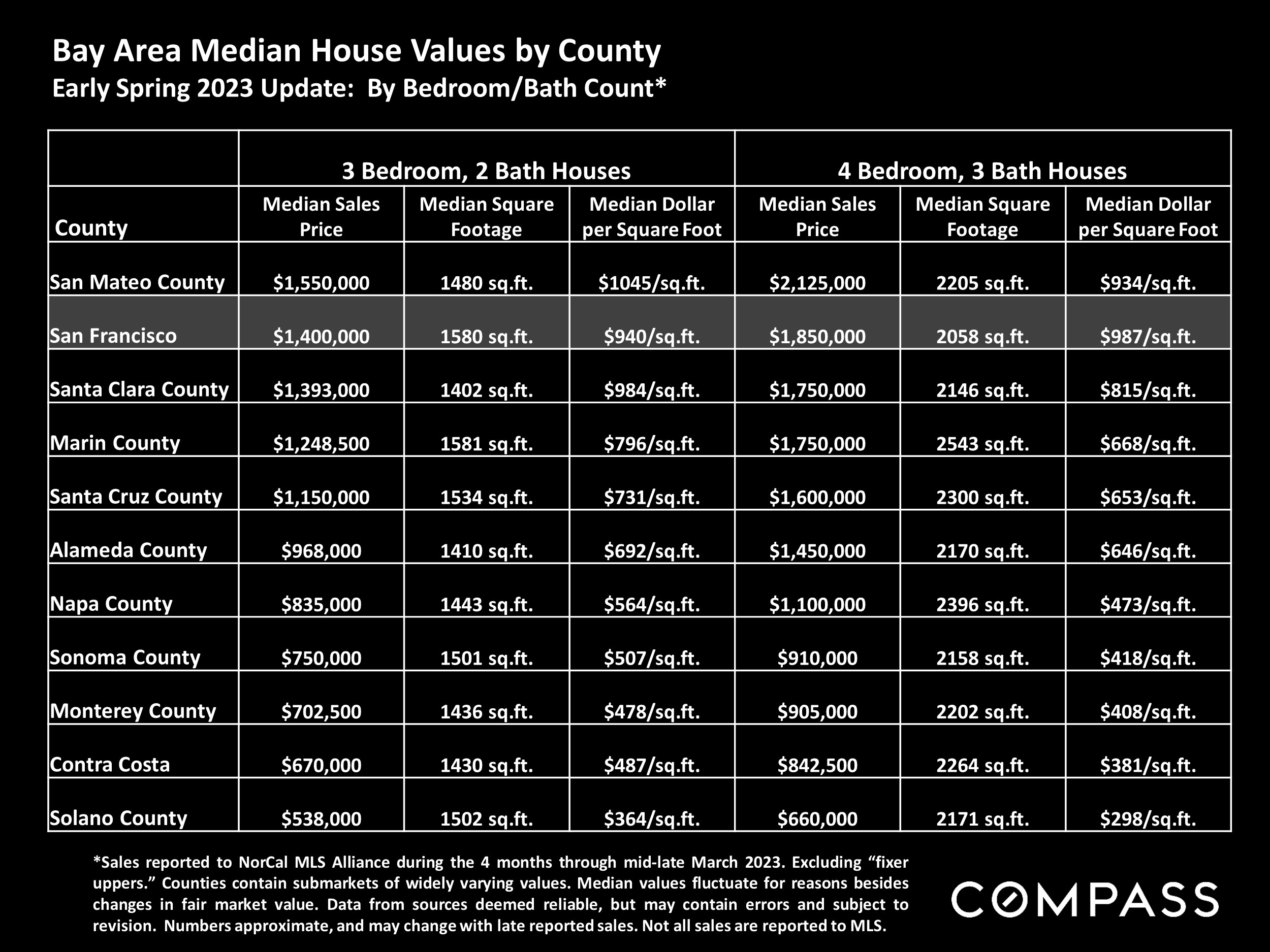

Many aspects of value cannot be adequately reflected in median and average statistics: curb appeal, age, condition, amenities, views, lot size, quality of outdoor space, "bonus" rooms, additional parking, quality of location within the neighborhood, and so on. How any of these statistics apply to any particular home is unknown without a specific comparative market analysis.

|

|

Compass is a real estate broker licensed by the State of California operating under multiple entities. License Numbers 01991628, 1527235, 1527365, 1356742, 1443761, 1997075, 1935359, 1961027, 1842987, 1869607, 1866771, 1527205, 1079009, 1272467. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions.

|

|

|

|

|

|

|