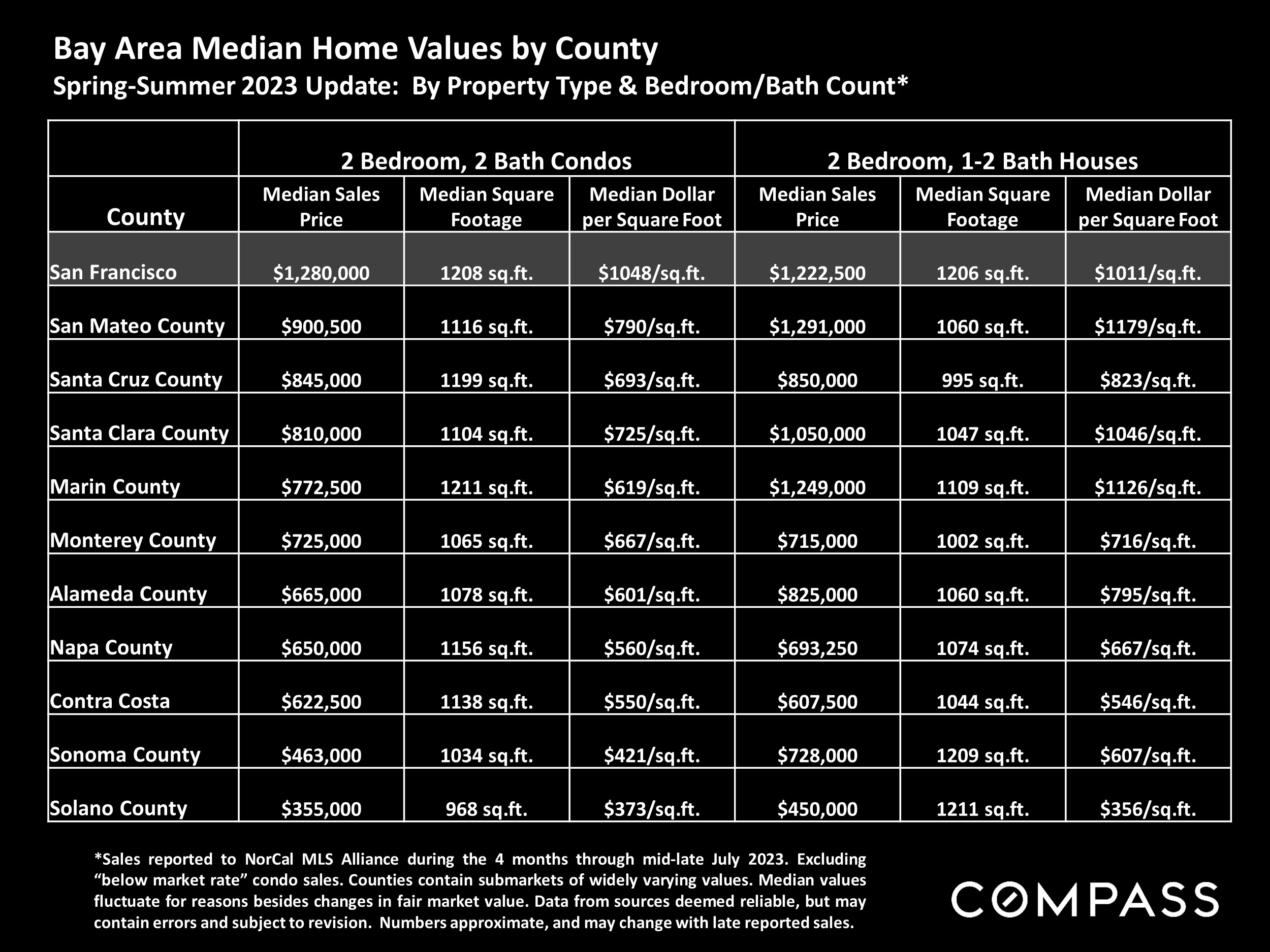

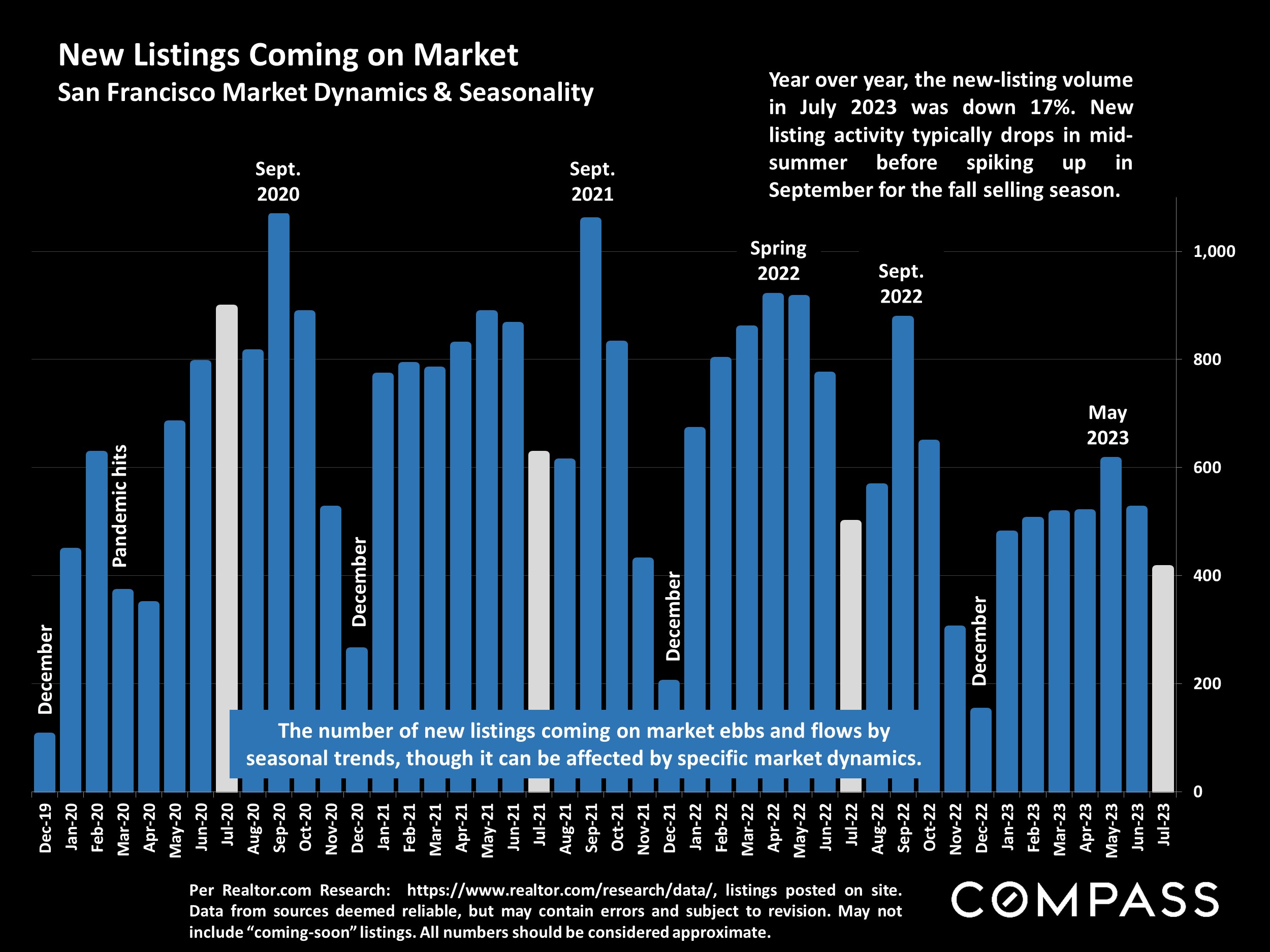

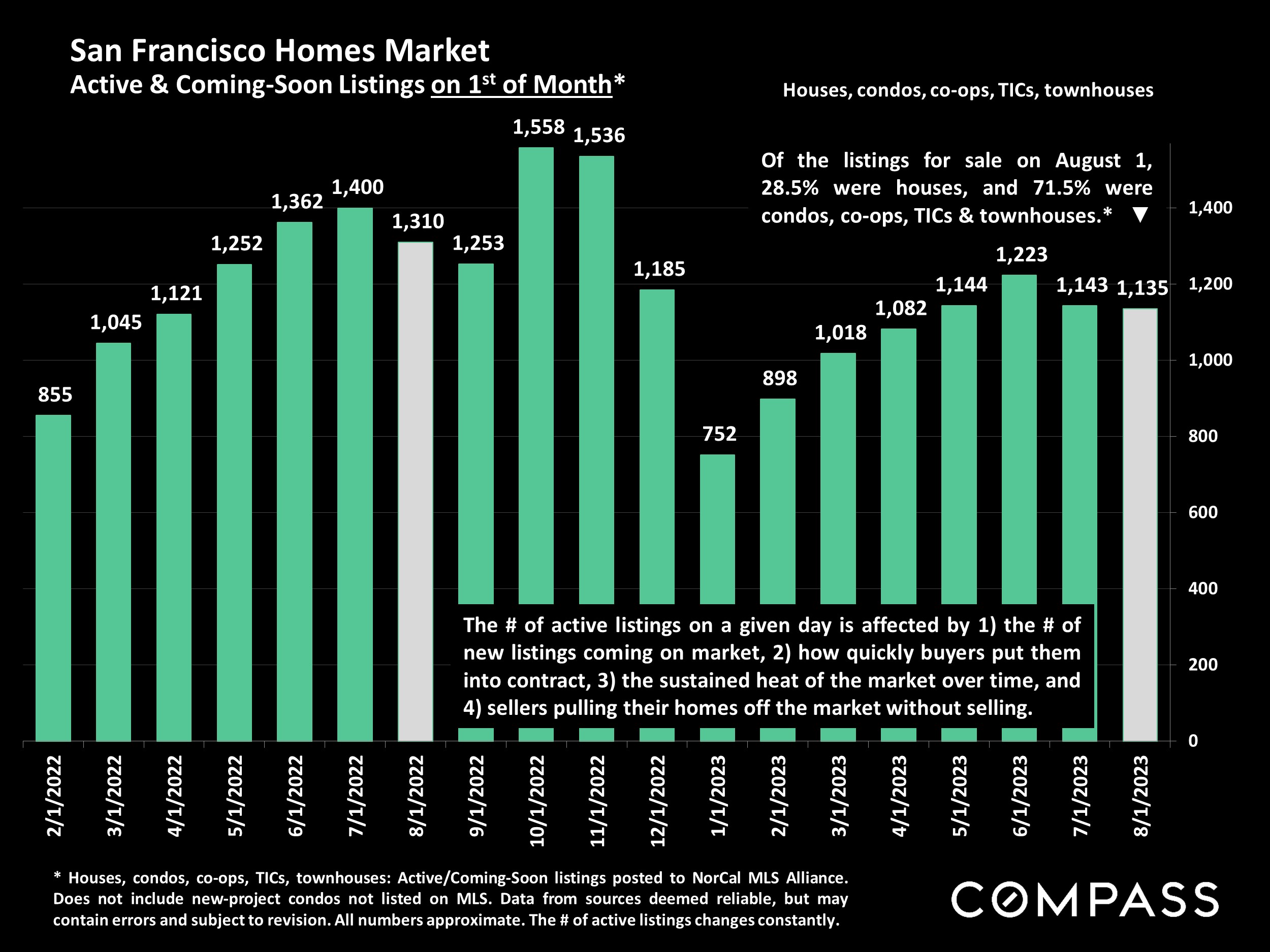

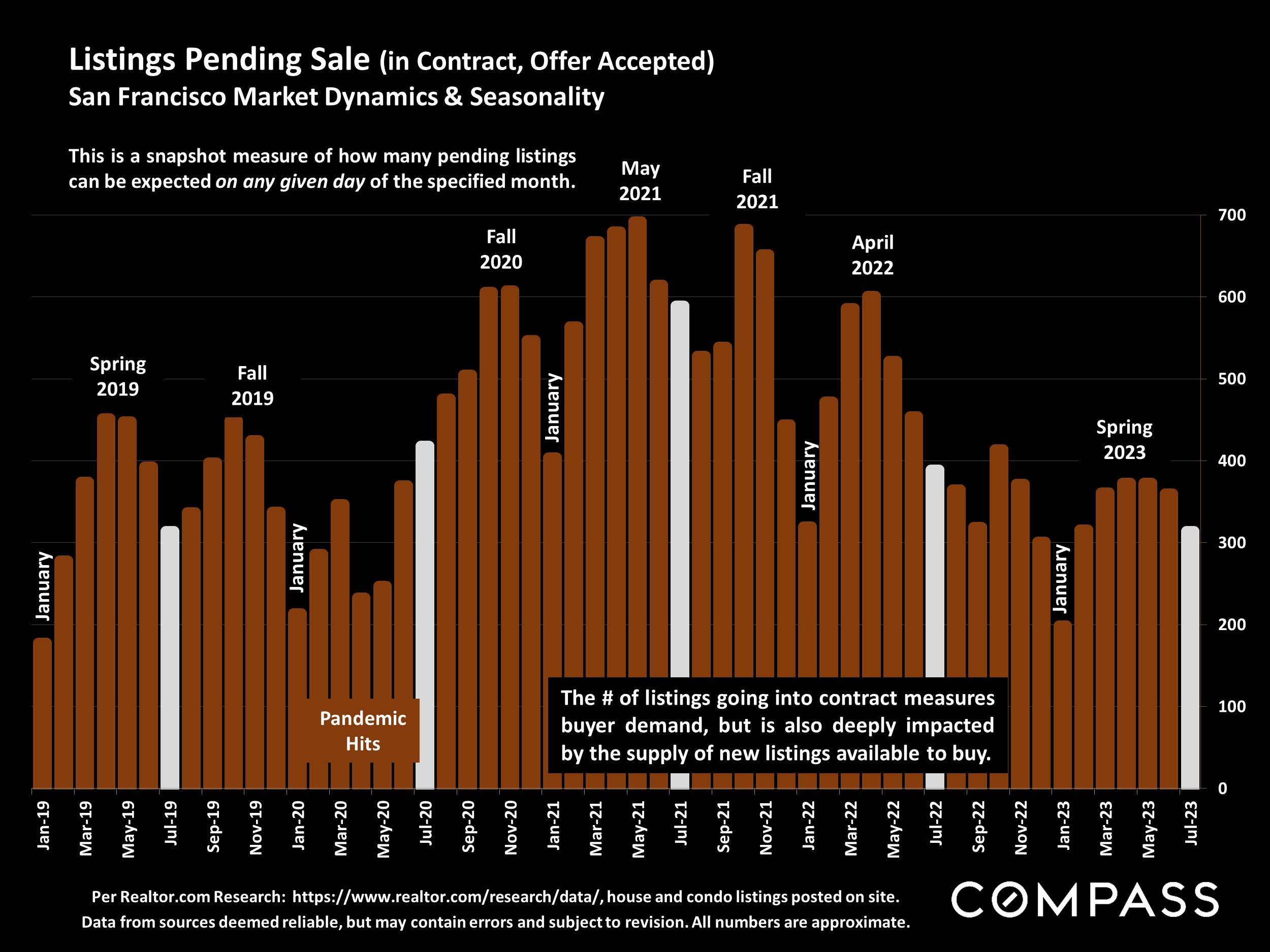

|

|

Friends, clients, and colleagues:

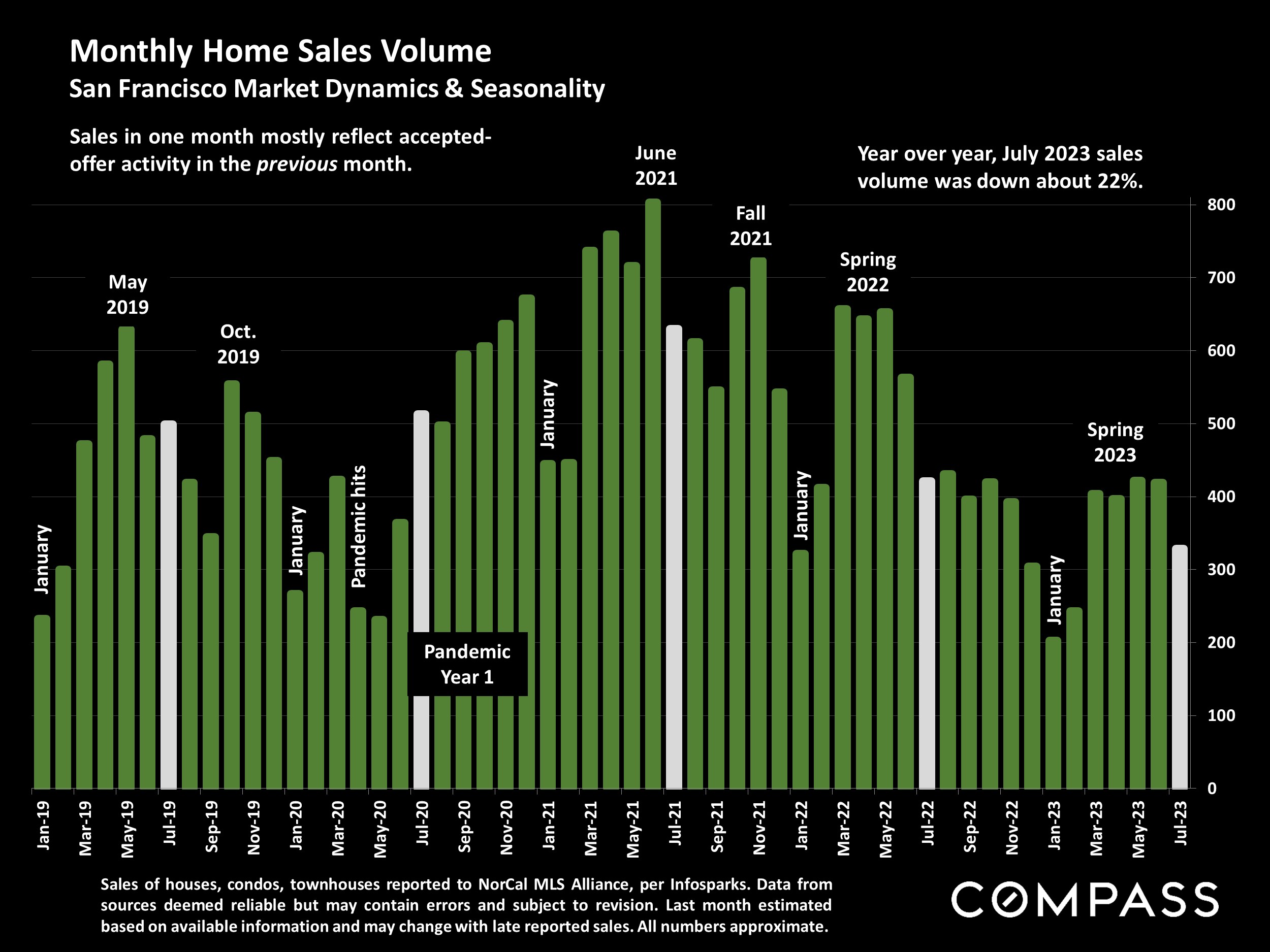

As we navigate the seasonally slower market here in summer, there's a growing optimism as it relates to San Francisco real estate. I'm climbing aboard and I'm going to tell you why.

While there's many elements at play, there's always been 2 primary factors impacting our market here in San Francisco: remote work & interest rates.

SF has a long way to go with regards to office space and general foot-traffic, but with (a) reports of more local companies requiring employees to come back to the office (on a hybrid schedule), and (b) a 10% increase in office demand in Q2 (according to VTS, a commercial real estate tech firm), it feels safe to say the worst is probably behind us.

San Francisco saw a 38% year-over-year increase in visits to office buildings throughout SF, marking the biggest recovery in office foot traffic in July across an 11-city study conducted by Placer.ai.

But, obviously, this isn't to say that is SF is back to what it was.

San Francisco's office foot traffic remains down nearly 56% from July 2019. This trails nationwide metrics, where office visits remain down 37% from July 2019.

The other pertinent news here is the AI industry and their appetite for San Francisco. Bigger real estate stakeholders in SF are beginning to dub the adjoining points of Mission, western SoMa, and Potrero Hill as "Area AI." (I remember when they tried to dub this region as SoMissPo about 5 years back, LOL).

Adept AI Labs is currently looking to add an additional 35,000sqft of office space in the area, adding to more than two dozen companies in the neighborhood that are classified as AI (per real estate firm JLL).

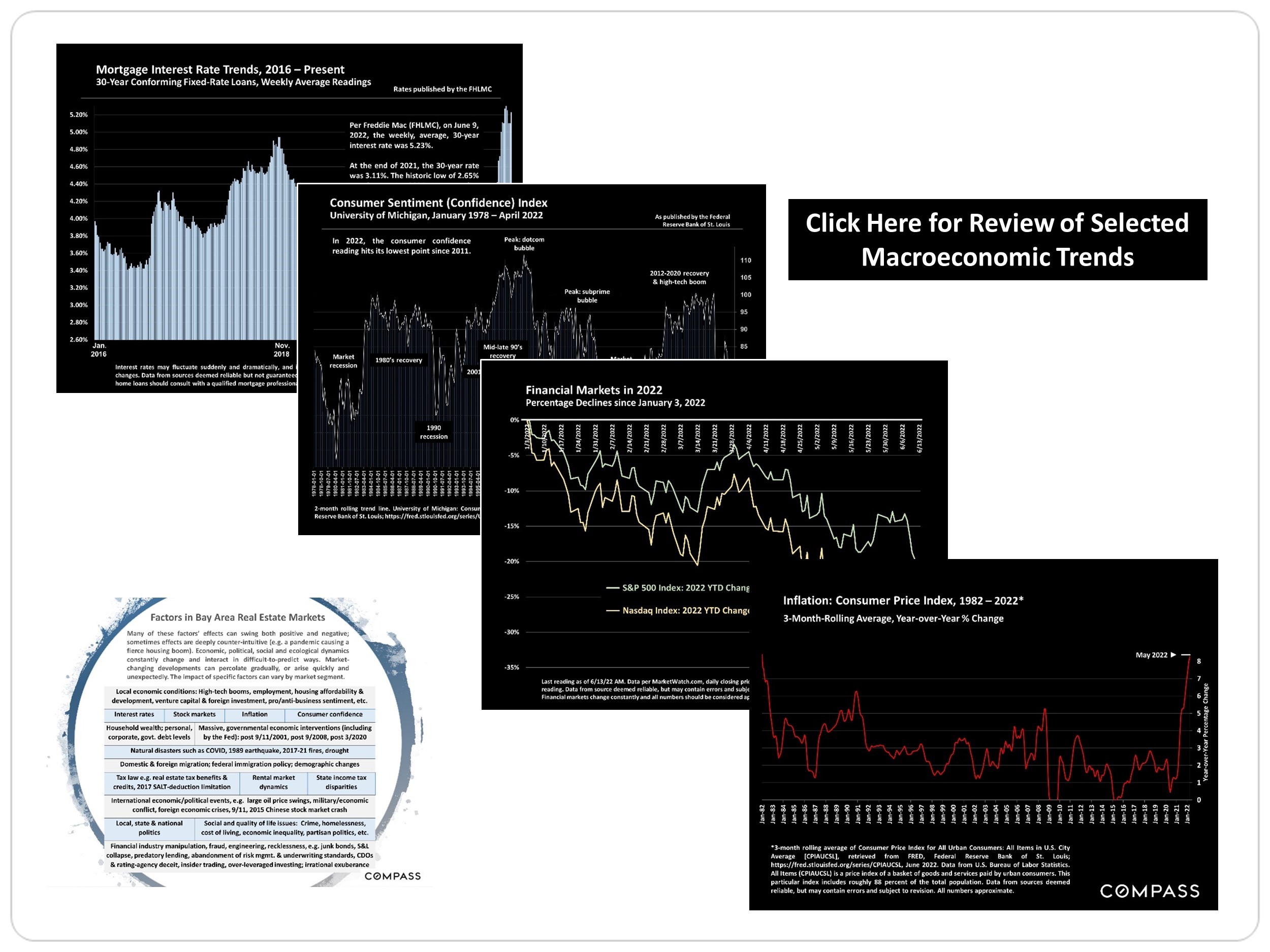

Among all the factors you can name as it relates to San Francisco real estate, there's no doubt that interest rates are the most impactful. Regardless of what else is happening in this city, if/when interest rates start dropping, activity meaningfully strengthens.

The 30-year fixed is currently at ~7.25%, still a very high figure in recent history. However there is a lot of positive news with the most recent inflation report.

"There are a lot of seeds in this report (July inflation report) that suggest more disinflation to come. It probably means that we are at - or very close to - the peak on interest rates. We think we're at the top." per NYT (Laura Rosner-Warburton, a senior economist at MacroPolicy Perspectives, a research firm.

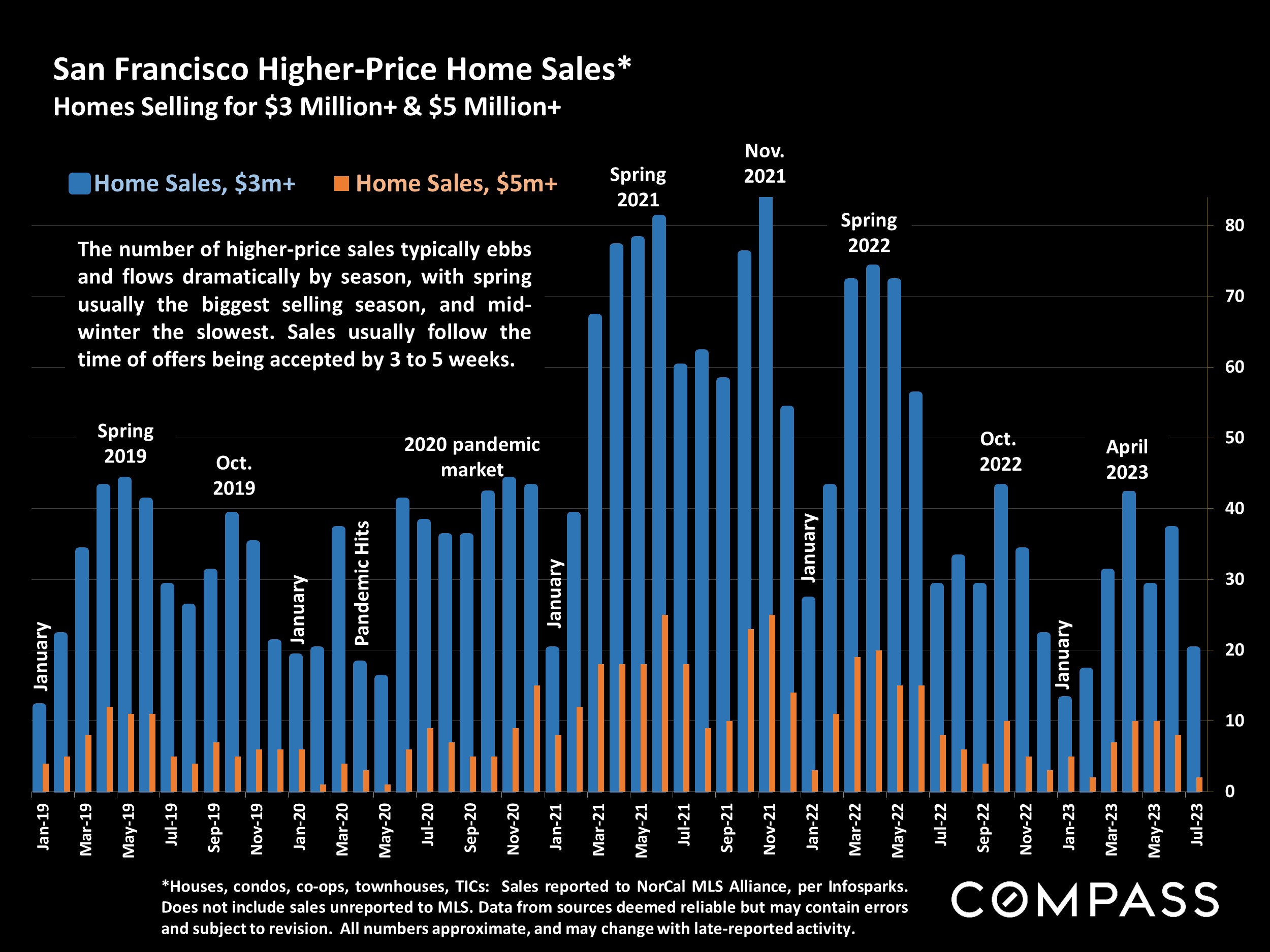

With the worst of remote work and interest rates most probably in the rearview mirror, it feels rational to predict that we're hovering right around the bottom of this market cycle. If you're in the downtown condo space, I'm actively assisting clients and seeing 20%+ discounts off pre-pandemic prices. If you're in the single-family or boutique condo space in our more classic SF neighborhoods (Russian Hill, Cow Hollow, Noe, Cole Valley, Pac Heights, NoPa, etc), you're likely to avoid competition and write a fair offer and terms. I recently helped a client purchase a large walk-up single-family in Noe with a deep, south-facing yard, and we were the only offer!

If you ever have any questions, I'm always here to help.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

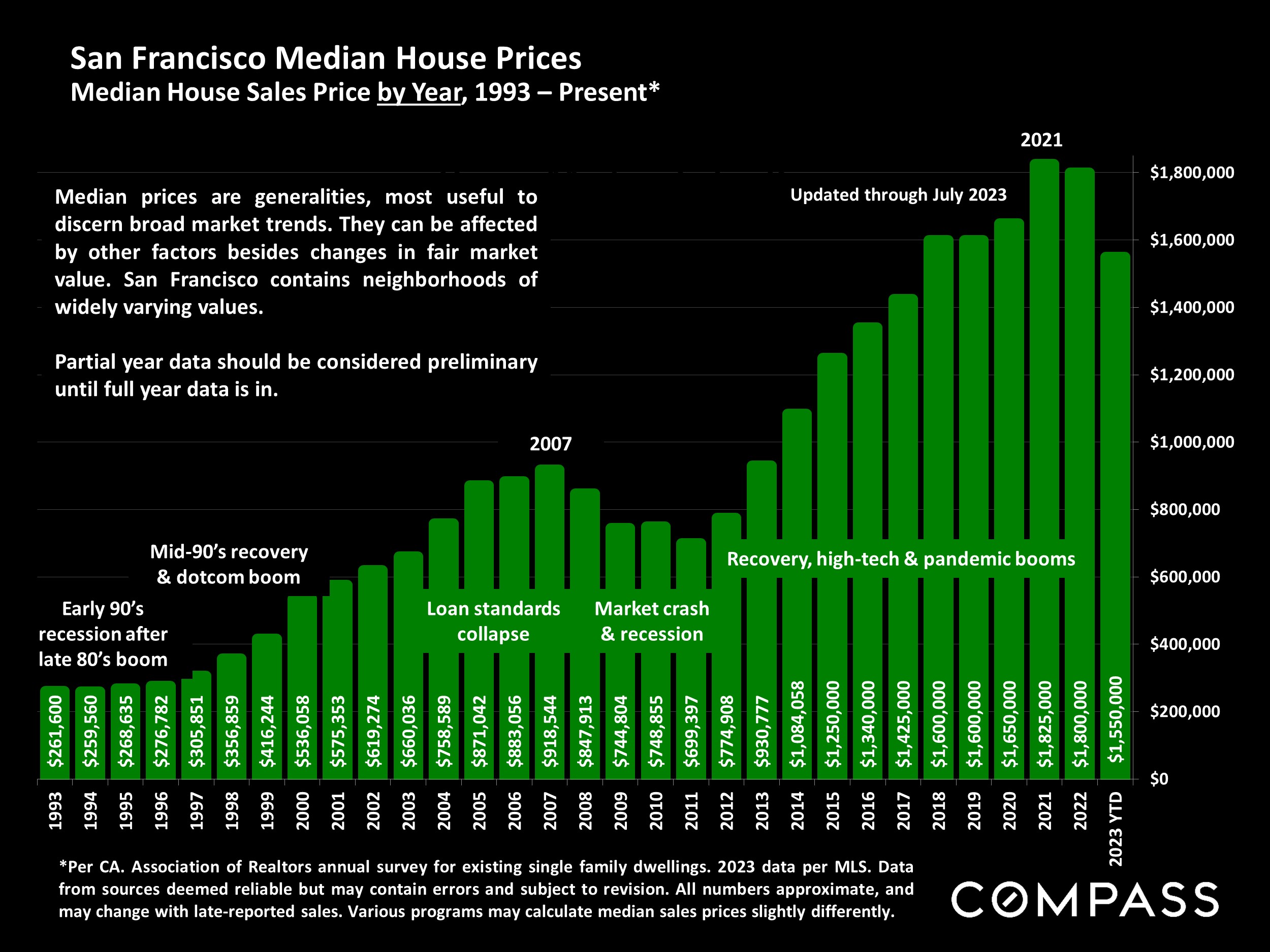

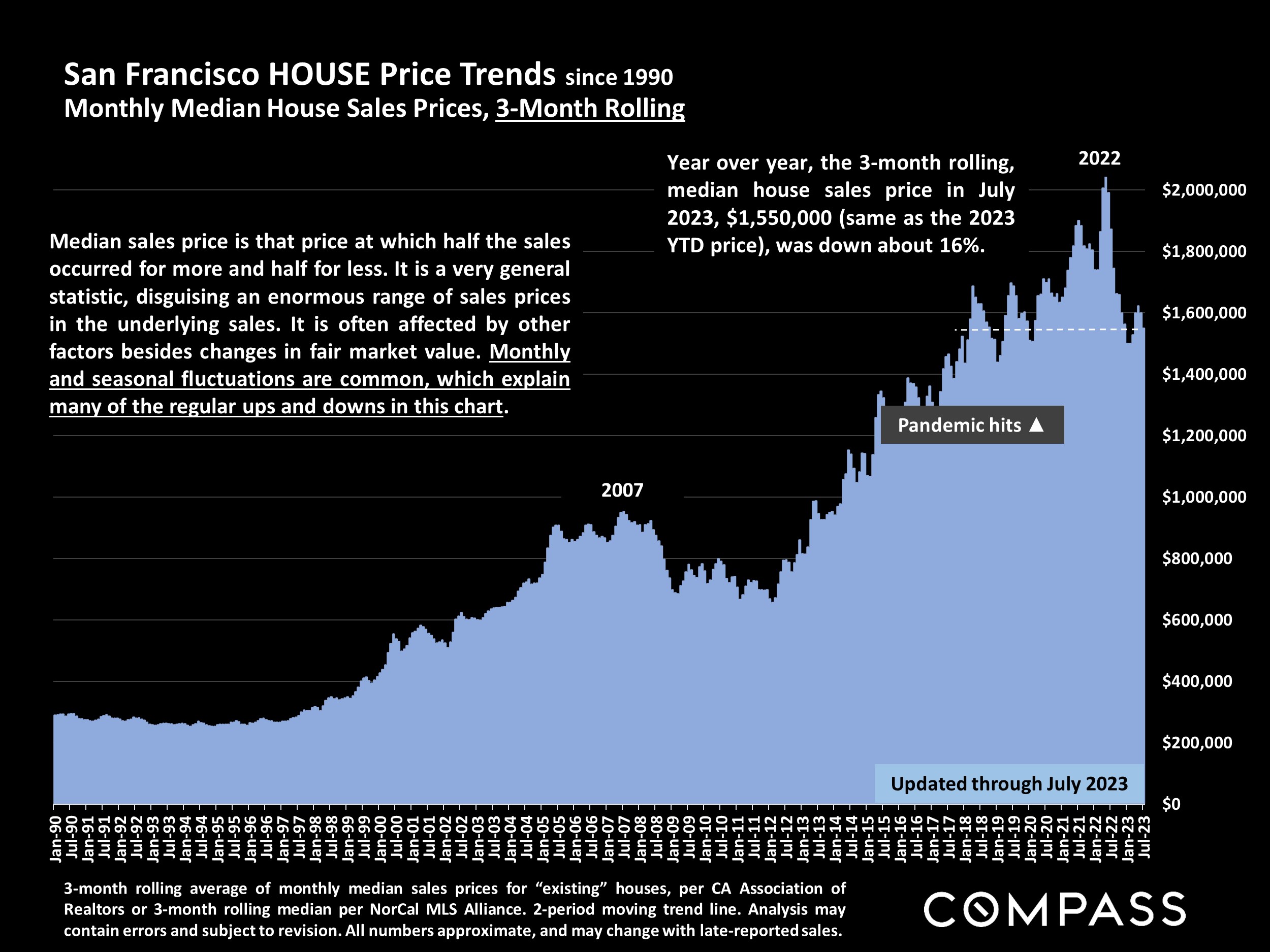

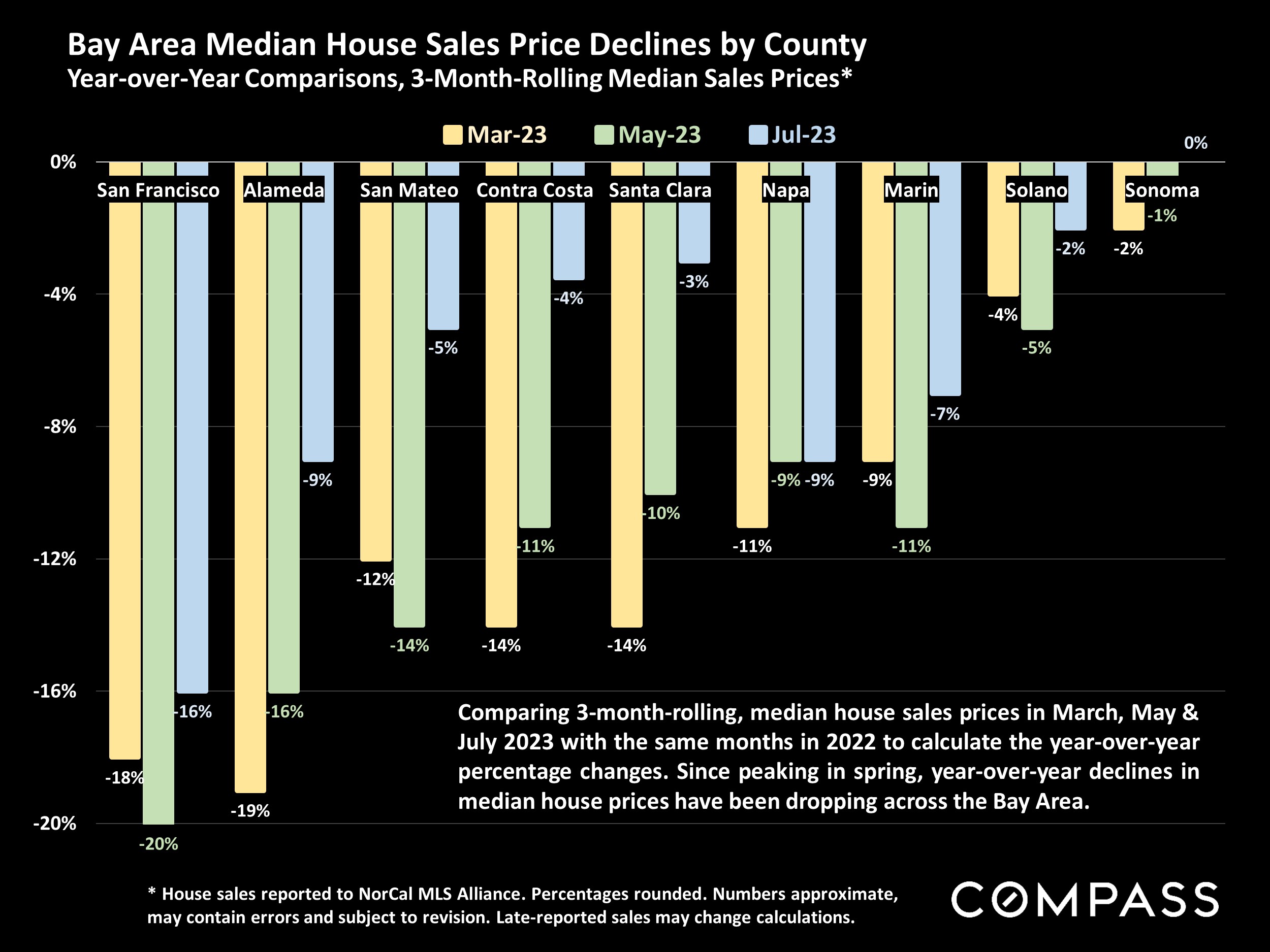

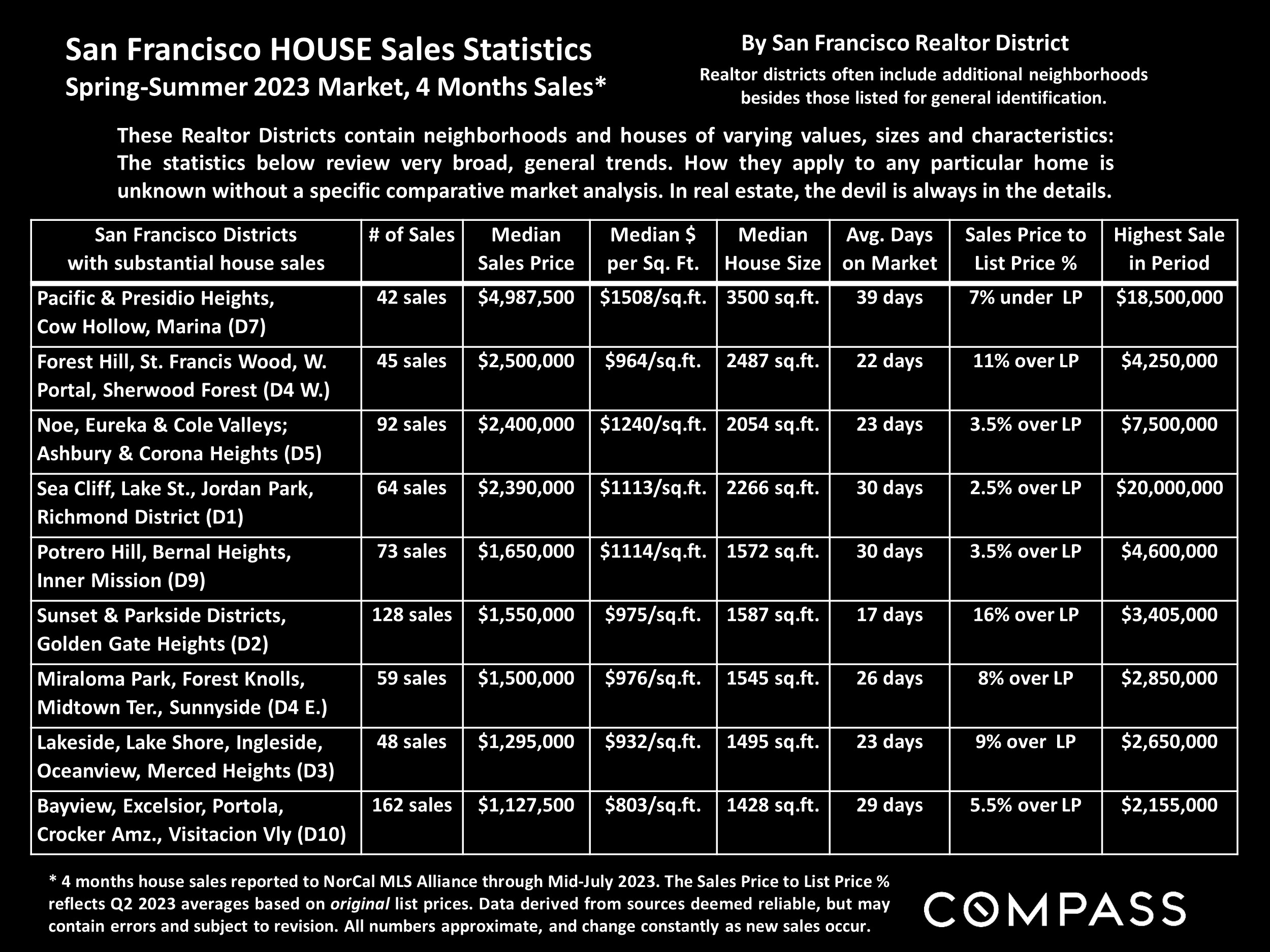

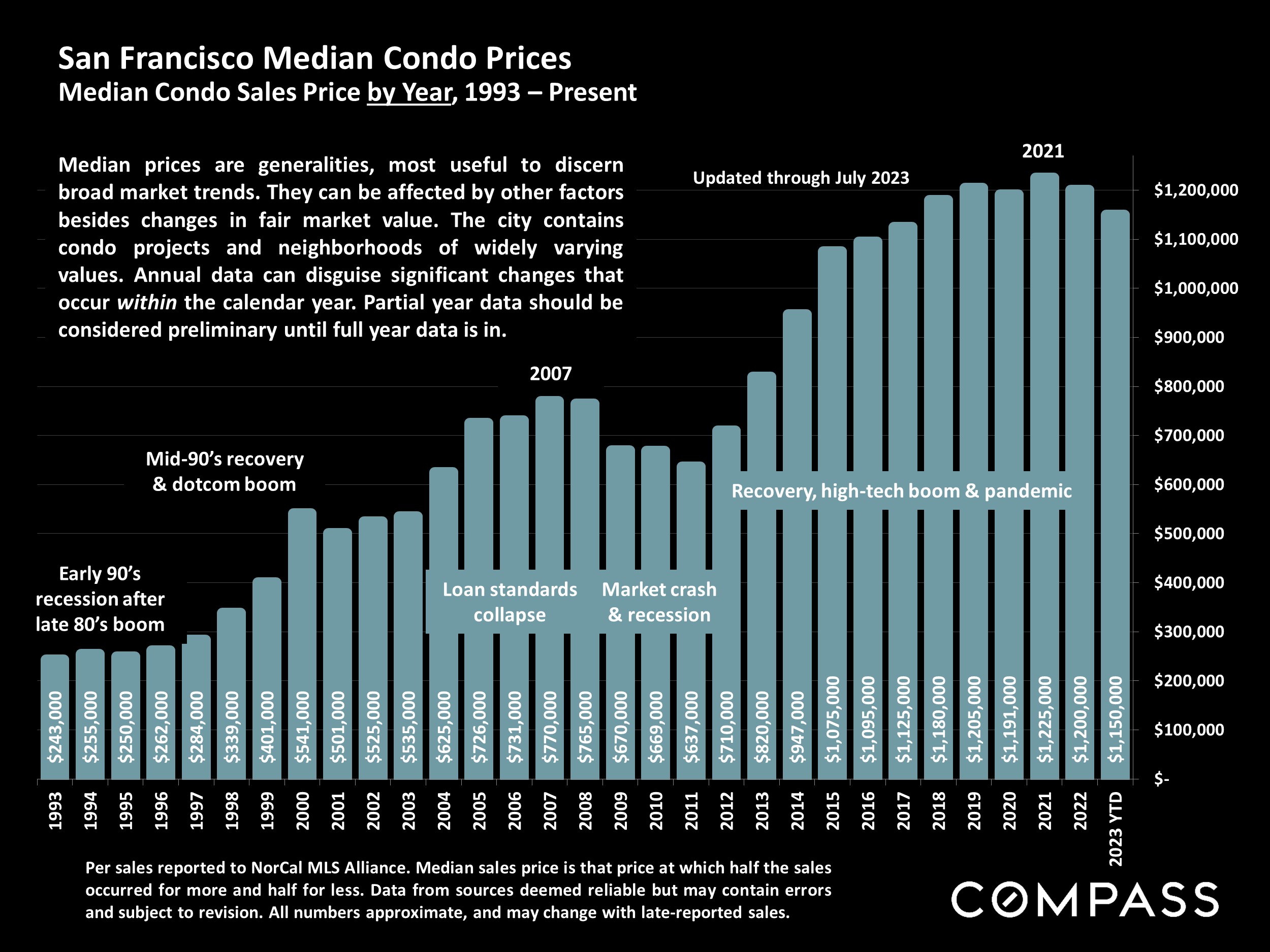

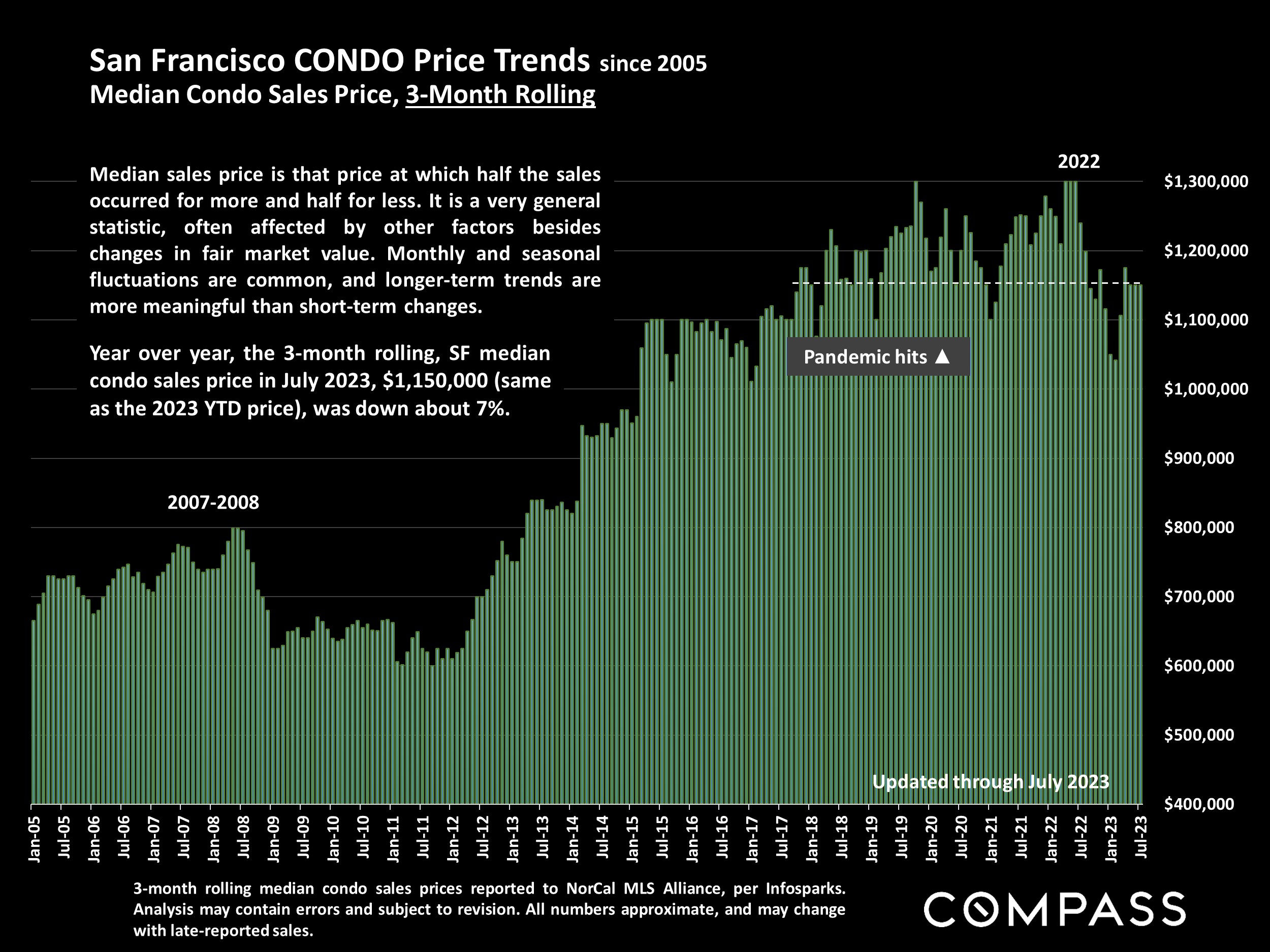

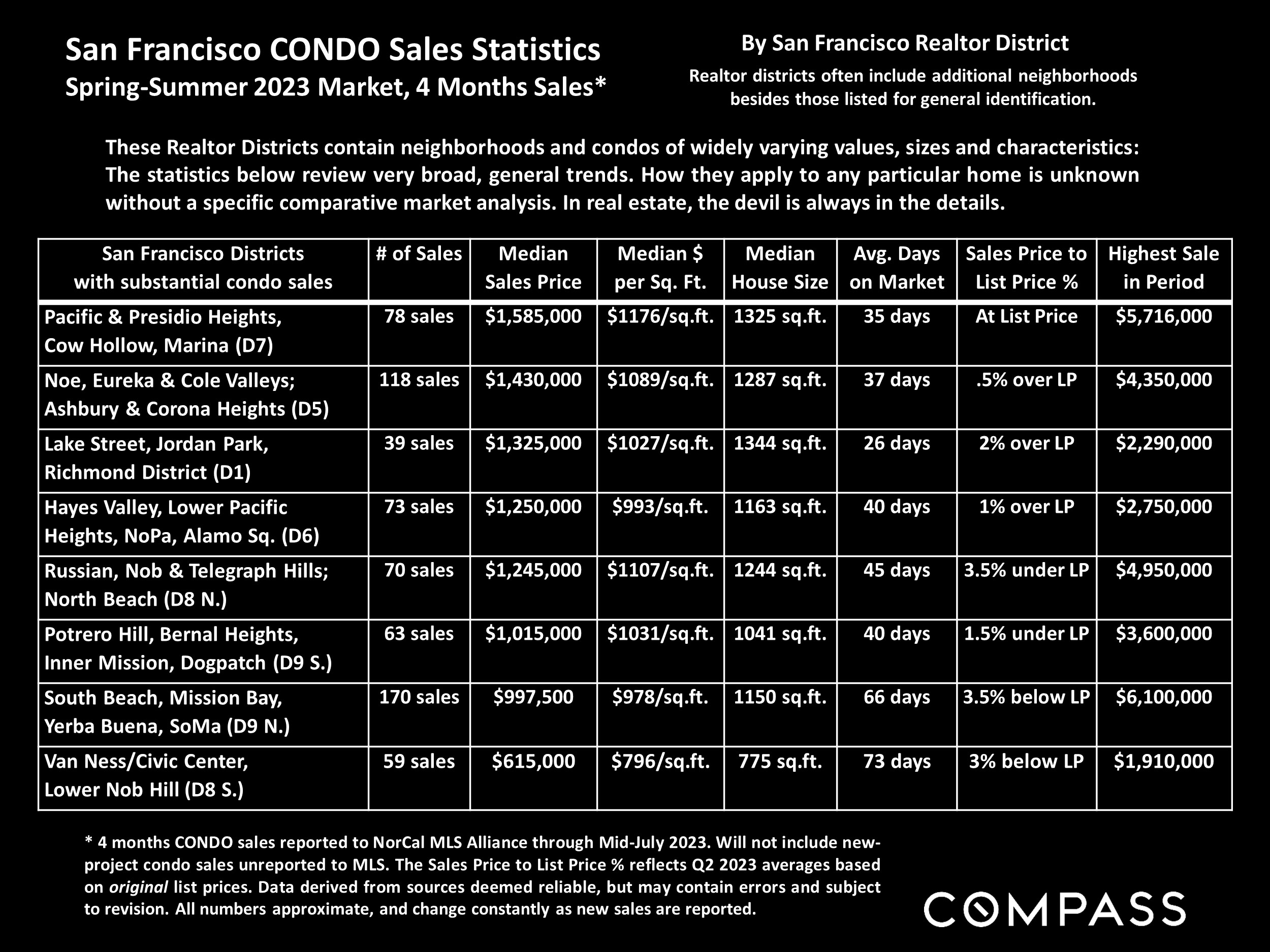

Statistics are generalities, essentially summaries of widely disparate data generated by dozens, hundreds or thousands of unique, individual sales occurring within different time periods. They are best seen not as precise measurements, but as broad, comparative indicators, with reasonable margins of error. Anomalous fluctuations in statistics are not uncommon, especially in smaller, expensive market segments. Last period data should be considered estimates that may change with late-reported data. Different analytics programs sometimes define statistics - such as "active listings," "days on market," and "months supply of inventory" - differently: what is most meaningful are not specific calculations but the trends they illustrate. Most listing and sales data derives from the local or regional multi-listing service (MLS) of the area specified in the analysis, but not all listings or sales are reported to MLS and these won't be reflected in the data. "Homes" signifies real-property, single-household housing units: houses, condos, co-ops, townhouses, duets and TICs (but not mobile homes), as applicable to each market. City/town names refer specifically to the named cities and towns, or their MLS areas, unless otherwise delineated. Multicounty metro areas will be specified as such. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers to be considered approximate.

Many aspects of value cannot be adequately reflected in median and average statistics: curb appeal, age, condition, amenities, views, lot size, quality of outdoor space, "bonus" rooms, additional parking, quality of location within the neighborhood, and so on. How any of these statistics apply to any particular home is unknown without a specific comparative market analysis.

|

|

Compass is a real estate broker licensed by the State of California operating under multiple entities. License Numbers 01991628, 1527235, 1527365, 1356742, 1443761, 1997075, 1935359, 1961027, 1842987, 1869607, 1866771, 1527205, 1079009, 1272467. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions.

|

|

|

|

|

|

|