Clients, friends, and colleagues:

If you’re only looking at headlines, it would be easy to conclude that the San Francisco market is completely out of reach right now. Prices are pushing past prior peaks, competition is intense, and the luxury segment is moving with real momentum. That part is true. But it’s also only part of the story.

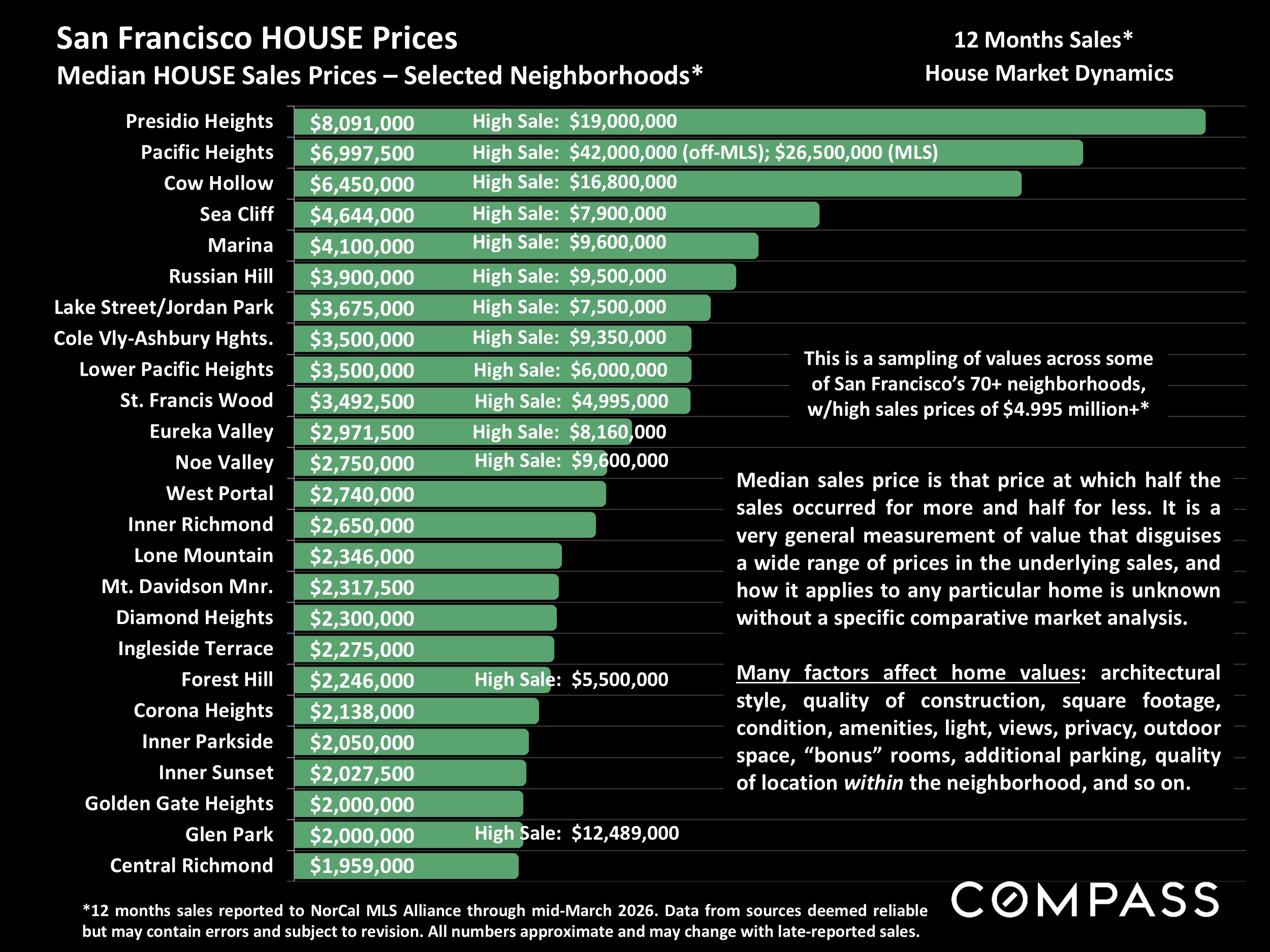

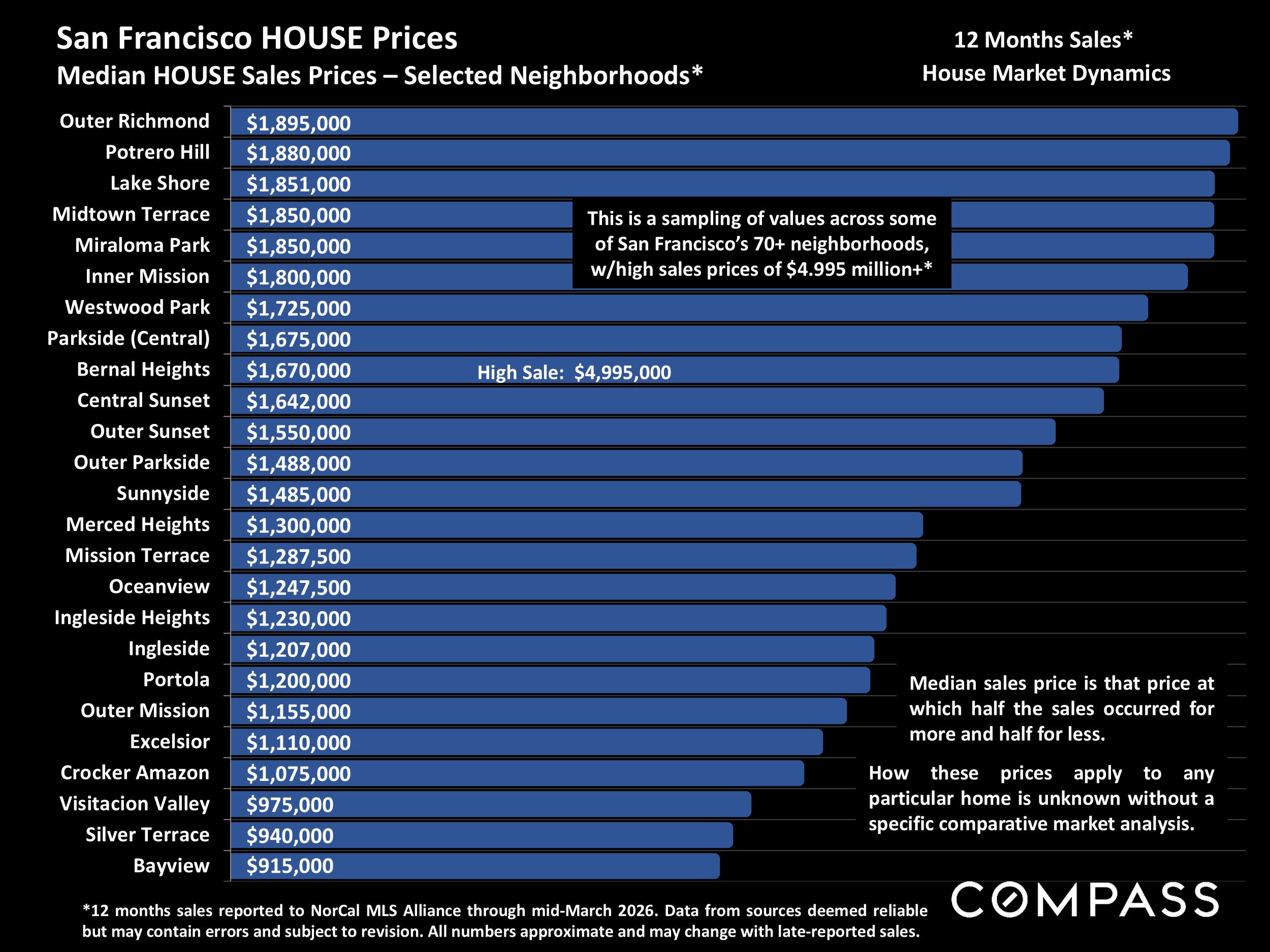

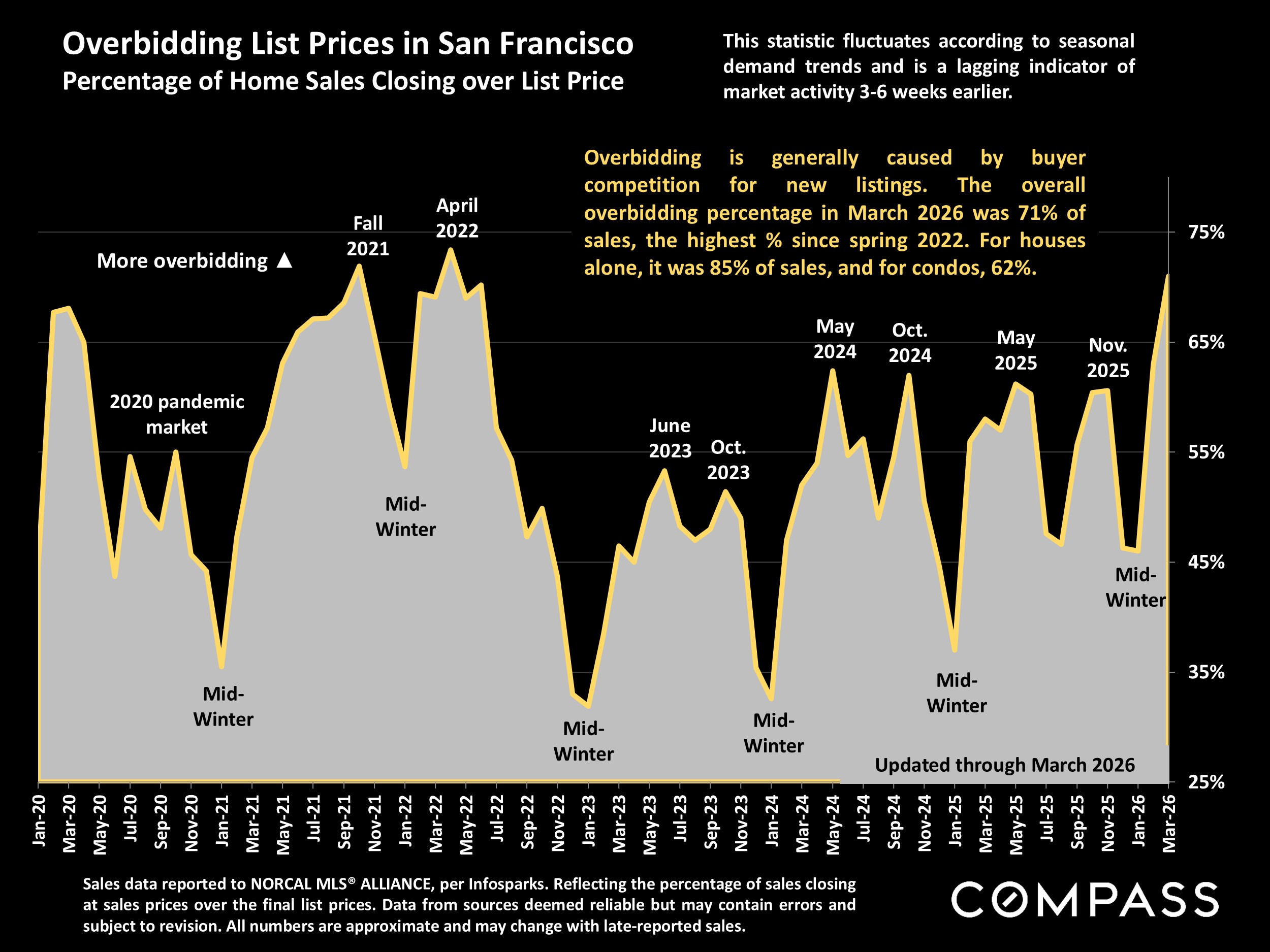

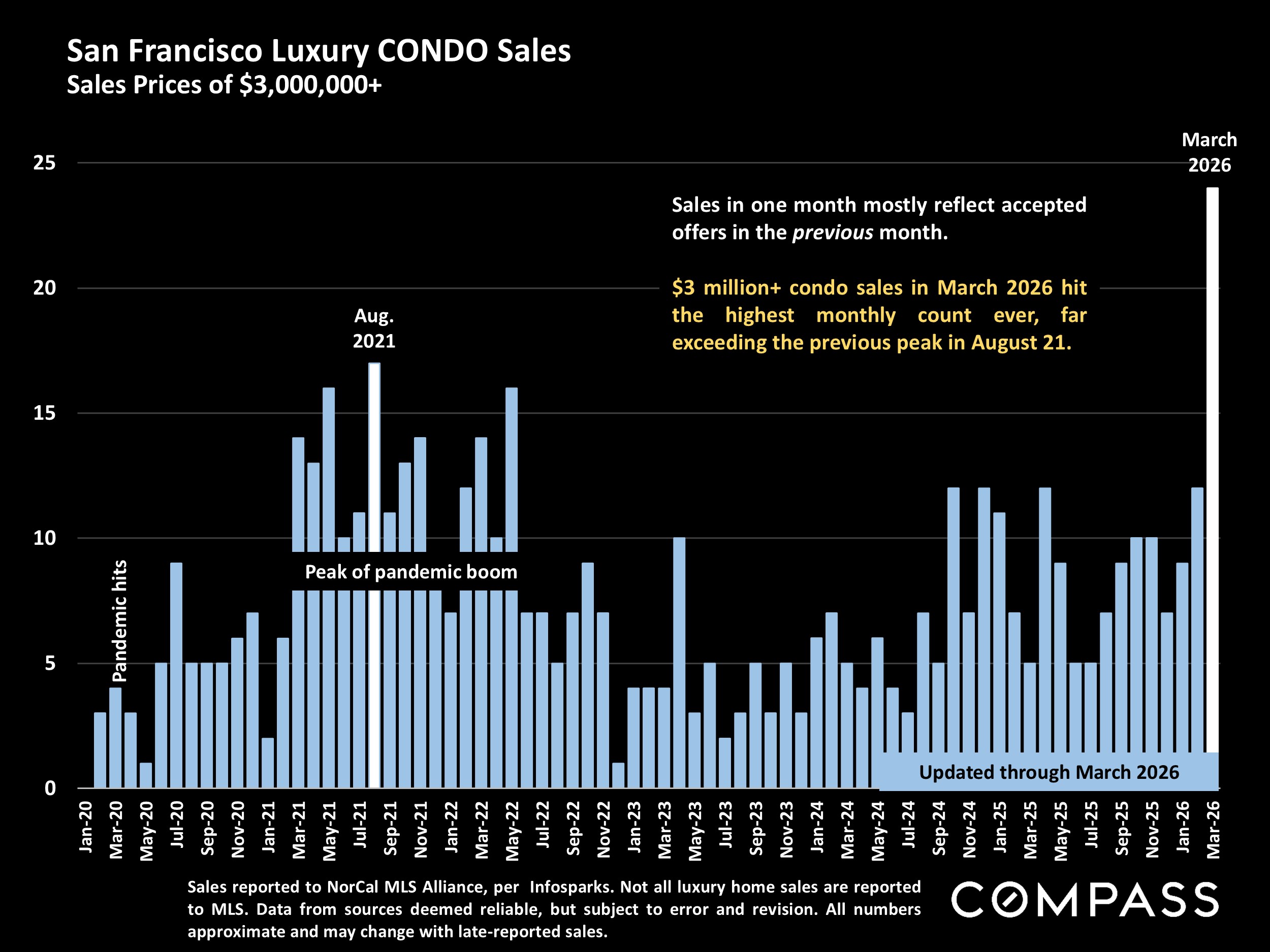

In March, the median house price reached $2,150,000, up 18% year over year and above the previous 2022 peak. Condo prices rebounded as well, with a median of $1,357,500, up 27% year over year and just under their all-time high. At the top end, activity has been especially strong, with $5M+ house sales up 83% year over year and $3M+ condo sales up 380%, both setting new highs. At the same time, supply remains tight, with new listings down 28% year over year, and that imbalance is showing up in competition. About 85% of houses are selling above asking, with an average overbid of 23%, while condos are coming in closer to 7% over.

Those numbers are real, but they’re also shaping a narrative that doesn’t fully reflect how most of the market is actually behaving.

What we’re seeing right now is really two markets operating at the same time. At the high end, capital is competing with capital. In many cases, cash is competing with cash, and outcomes are being driven by speed, certainty, and a willingness to remove friction. That’s what’s pushing prices higher and creating the sense that everything is overheated.

But below that, the dynamic is different. Properties under $2M, which account for the majority of transactions, are still active and competitive, but much more measured. It’s not unusual to see 15 to 30 disclosure packages go out and only a handful of offers come back. Buyers are engaged, but they’re more selective, more analytical, and more sensitive to pricing than they were a few years ago.

That shift largely comes down to the cost of capital. When rates were low, financing expanded the buyer pool and drove competition across almost every price point. Today, financing is still very much in the market, but it’s more disciplined. Buyers are underwriting more carefully, and that’s creating a wider gap between properties that are well-positioned and those that miss the mark. It’s also why, despite all the strong data, some listings are quietly sitting or falling through the cracks.

So while the luxury market is setting the tone, it isn’t defining the full landscape. San Francisco remains supply-constrained, demand remains durable, and well-positioned properties are still trading quickly, with median days on market around 12 for houses and 18 for condos. But success right now is less about reacting to the loudest signals and more about understanding where the conditions are actually different.

For buyers, that means there is still opportunity, but it requires focus and a clear strategy. For sellers, it means the market will reward precision. The right pricing and positioning can still produce exceptional outcomes, but there’s less room for error than the headlines suggest.

As always, feel free to reach out if you want to talk through how this applies to your specific situation.

Warmly,

Faye