Clients, friends, and colleagues:

Spring in San Francisco always brings a shift in energy, and you can feel it again right now, both in the city and in the housing market.

Over the past few weeks, I’ve been seeing something that feels different from most of the last couple of years. Buyers aren’t just browsing or waiting for the perfect scenario. They’re engaging, competing, and in many cases making decisions faster than they would have even six months ago. What’s notable is that this isn’t limited to perfect properties. Well-located, well-presented homes are still commanding strong attention, but even properties with tradeoffs are drawing multiple offers when the fundamentals make sense.

That’s usually how a market shift starts. The hesitation we’ve seen from buyers since interest rates jumped in 2022 is starting to soften, and the conversation is moving from “should I wait?” to “how do I win this?”

You can start to see it show up in pricing as well. In Noe Valley, well-positioned single-family homes are now trading close to $2,000 per square foot. In the Inner Sunset, fully renovated homes are pushing toward $1,600 per square foot when they are dialed in and move-in ready. And in Pacific Heights, single-family homes with dramatic views and top-tier finishes are beginning to break into the $3,000 per square foot range. These numbers don’t appear everywhere at once, but they tend to surface first in neighborhoods where demand historically leads the market.

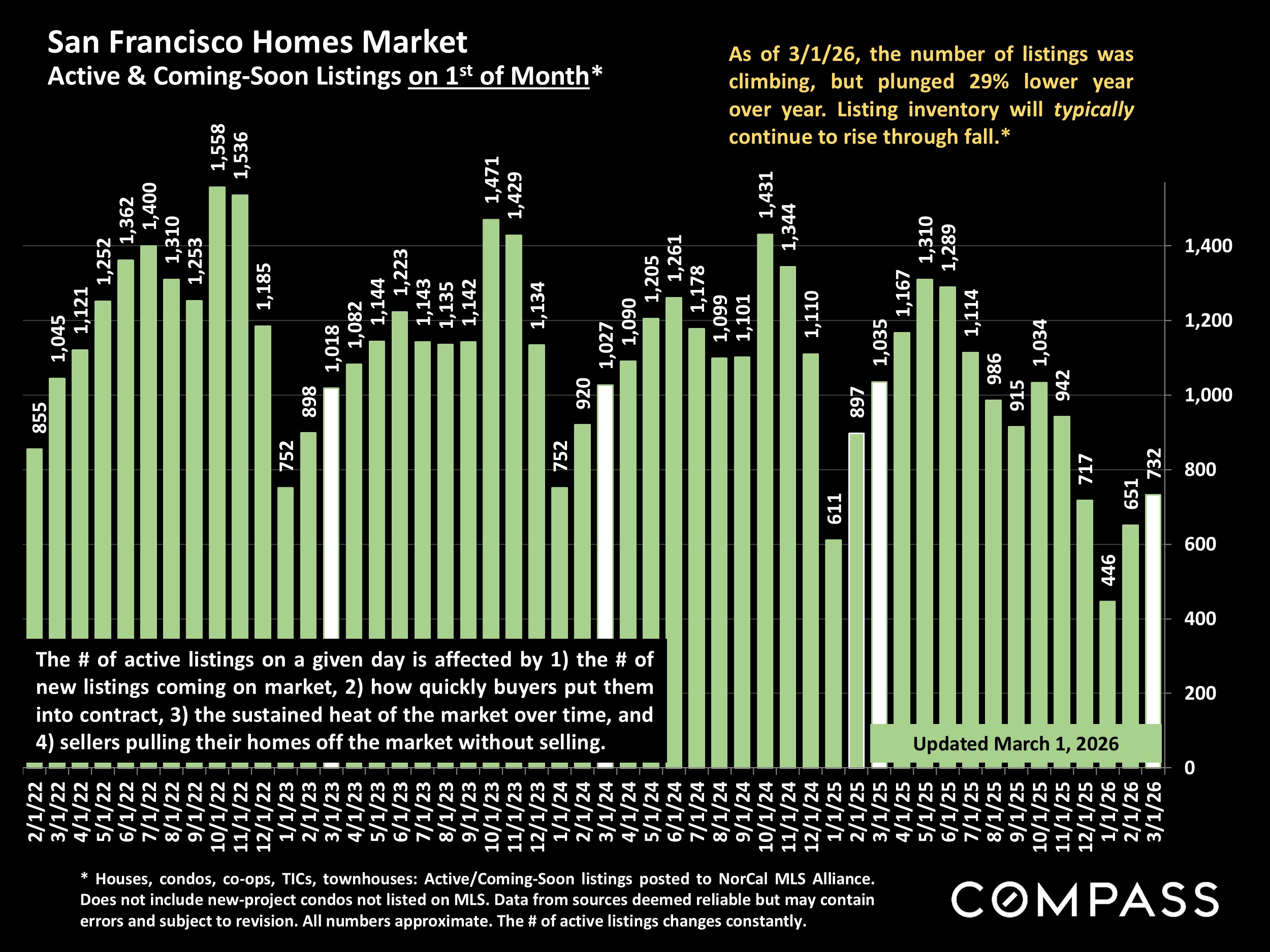

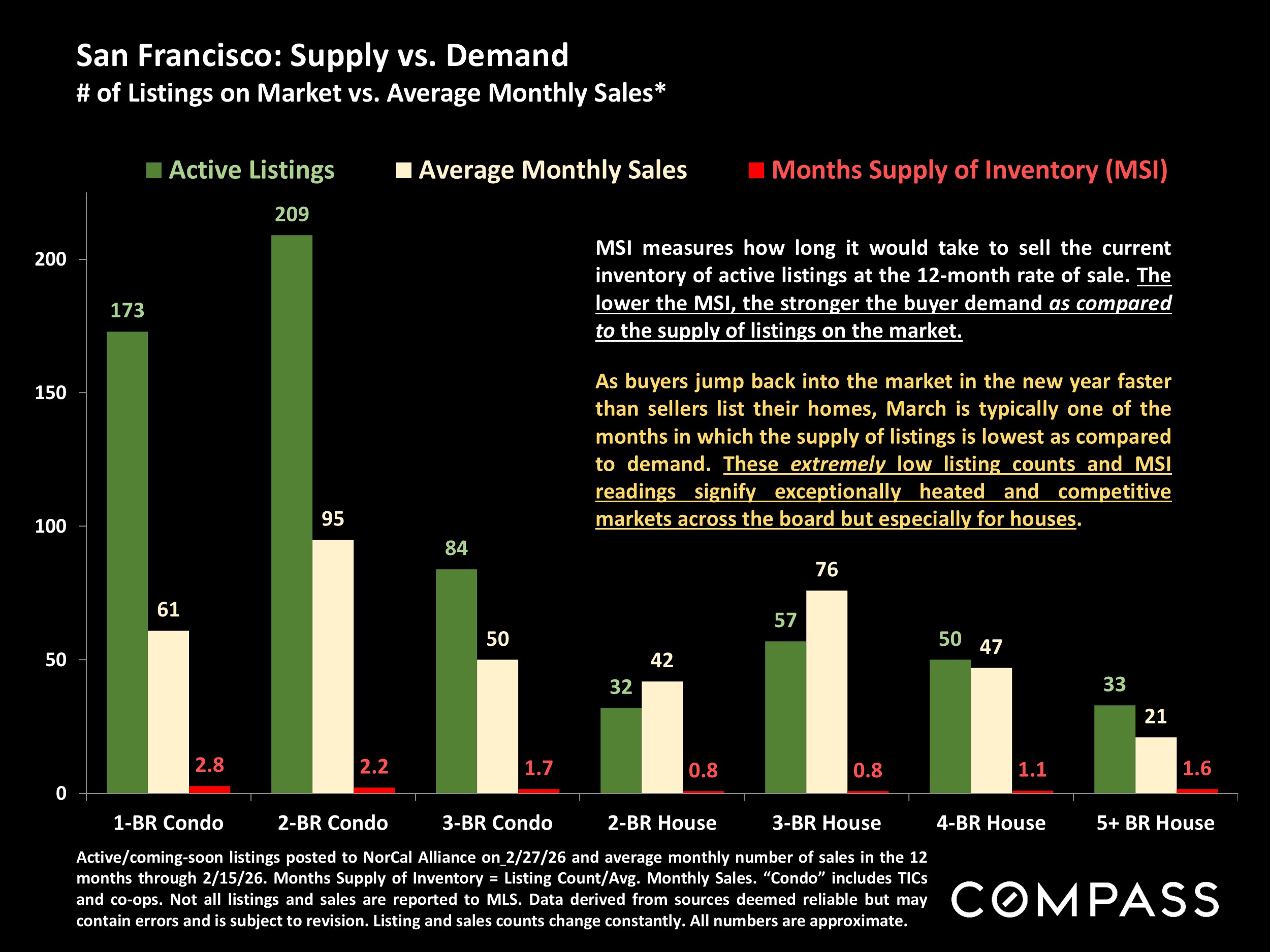

Zooming out, the broader data is now beginning to reflect what’s happening on the ground. Demand is picking up at a time when inventory remains constrained, which is leading to increased competition, faster sales, and upward pressure on pricing, especially in the single-family home segment. The condo market is also clearly participating in the rebound. At the higher end, activity has been particularly strong, with a notable surge in luxury sales and affluent buyers continuing to drive a disproportionate share of the market.

The upcoming months are typically among the most active of the year, and median home sales prices often hit their calendar-year highs in spring. Unless there is a meaningful shift in the macro environment, the current trajectory suggests a competitive season ahead.

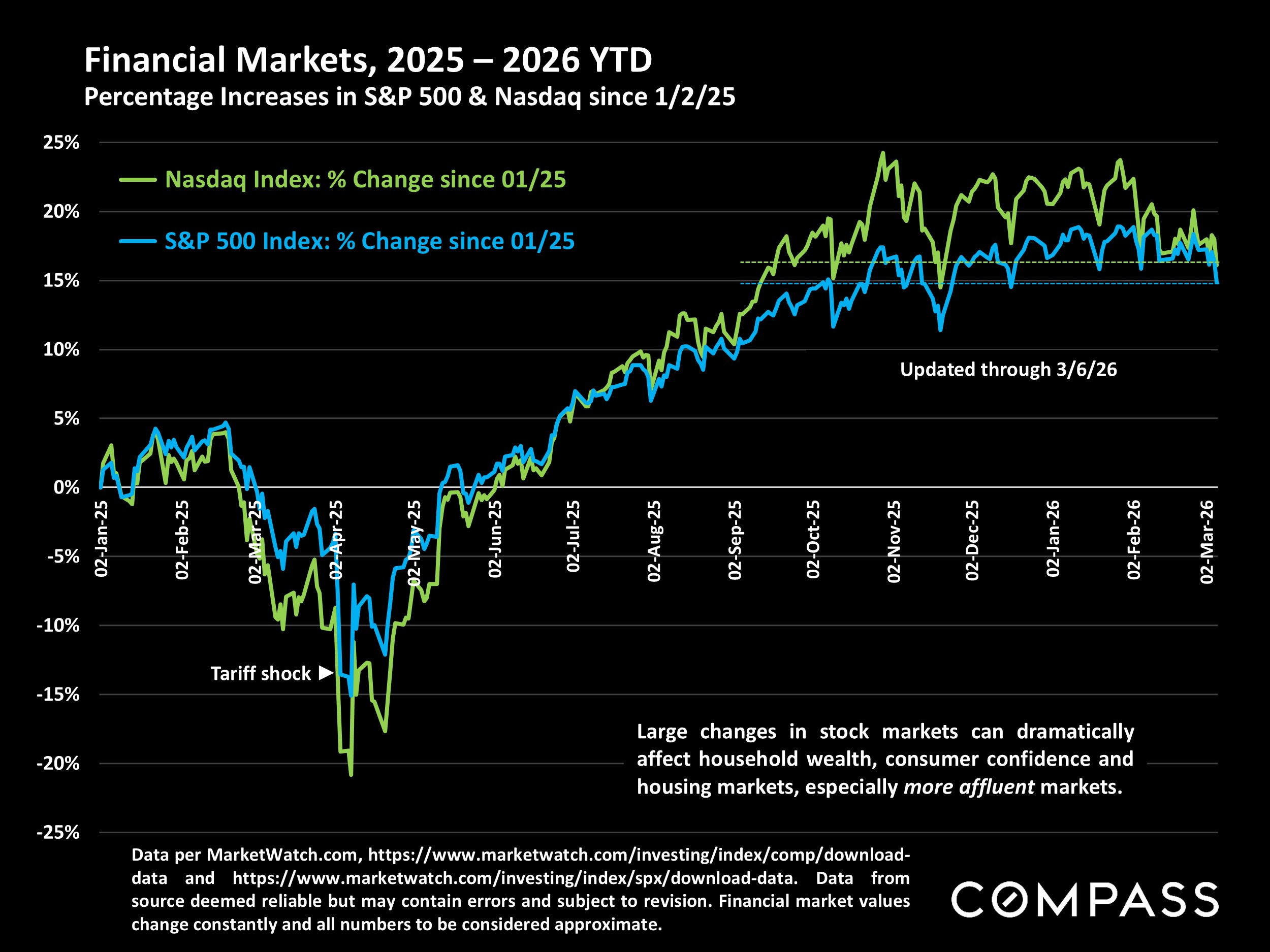

The wild card in coming months is what sustained effects, if any, the Iran war may have on inflation, interest rates, financial markets and consumer confidence. Barring an extreme decline in economic conditions, we currently consider a significant negative impact on the city’s housing market unlikely.

Cheers,

Faye